Antero Resources | CNX Resources | Commodity Price | Coterra Energy (Cabot O&G) | Energy Companies | EQT Corp | Gulfport Energy | Industrywide Issues | Range Resources Corp | Southwestern Energy

Marcellus/Utica Driller Stock Prices Trend Up with NatGas Price

We spotted a couple of stories, one in Barron’s the other in the Wall Street Journal, about the pickup in the futures price of natural gas over the past week, and how those recent gains have led to impressive gains in the share price for Marcellus/Utica drillers. Yesterday the NYMEX Henry Hub futures price closed up 4.11% to $2.74/Mcf. The rising tide lifts all boats.

We spotted a couple of stories, one in Barron’s the other in the Wall Street Journal, about the pickup in the futures price of natural gas over the past week, and how those recent gains have led to impressive gains in the share price for Marcellus/Utica drillers. Yesterday the NYMEX Henry Hub futures price closed up 4.11% to $2.74/Mcf. The rising tide lifts all boats.

Read More “Marcellus/Utica Driller Stock Prices Trend Up with NatGas Price”

Have you caught yourself thinking lately (as we have), “When in the world is the price of natural gas (and oil) going to go up again?” And, “Why is more drilling not happening?” Perhaps you answer yourself with the obvious answer: It’s the pandemic, stupid. If you have said/thought that, you are correct. But what is there about the pandemic (which seems to be getting better) that is causing this ongoing slowdown and low prices for oil and gas?

Have you caught yourself thinking lately (as we have), “When in the world is the price of natural gas (and oil) going to go up again?” And, “Why is more drilling not happening?” Perhaps you answer yourself with the obvious answer: It’s the pandemic, stupid. If you have said/thought that, you are correct. But what is there about the pandemic (which seems to be getting better) that is causing this ongoing slowdown and low prices for oil and gas? If you live in New York City, Boston, or anywhere in the states of New Jersey, Massachusetts, Connecticut, Rhode Island, or New Hampshire, brace yourselves to pay much higher prices for your natural gas this winter. That’s according to an analysis by S&P Global Platts. Right now the forward strip prices at key trading hubs in those locations show prices for natural gas in the range of $6.00-$6.63 per thousand cubic feet (Mcf), about twice the price of last winter.

If you live in New York City, Boston, or anywhere in the states of New Jersey, Massachusetts, Connecticut, Rhode Island, or New Hampshire, brace yourselves to pay much higher prices for your natural gas this winter. That’s according to an analysis by S&P Global Platts. Right now the forward strip prices at key trading hubs in those locations show prices for natural gas in the range of $6.00-$6.63 per thousand cubic feet (Mcf), about twice the price of last winter. Yesterday the price of natural gas trading on the NYMEX futures exchange, a price based on the spot price at the Louisana Henry Hub trading point, zoomed up, closing 30 cents higher than the trading day before (up 14%). There does not appear to be a single, specific reason why trading took off like wildfire. Some speculate it rose based on the good news that U.S. LNG exports are once again on the rise. Others say short-term forecasts are now predicting continued hot weather. Whatever the reason, we’ll take it!

Yesterday the price of natural gas trading on the NYMEX futures exchange, a price based on the spot price at the Louisana Henry Hub trading point, zoomed up, closing 30 cents higher than the trading day before (up 14%). There does not appear to be a single, specific reason why trading took off like wildfire. Some speculate it rose based on the good news that U.S. LNG exports are once again on the rise. Others say short-term forecasts are now predicting continued hot weather. Whatever the reason, we’ll take it! The experts at RBN Energy have been analyzing pipelines and natural gas flows out of the Marcellus/Utica region and warn of a coming problem this fall. Production in the M-U remains high. Storage is quickly filling up. The gas needs to exit the region in order to fetch better prices. According to RBN, “This fall, the situation could be even worse and may force producers to shut-in gas for a second time this year.” Pipeline constraints are coming, and that spells problems.

The experts at RBN Energy have been analyzing pipelines and natural gas flows out of the Marcellus/Utica region and warn of a coming problem this fall. Production in the M-U remains high. Storage is quickly filling up. The gas needs to exit the region in order to fetch better prices. According to RBN, “This fall, the situation could be even worse and may force producers to shut-in gas for a second time this year.” Pipeline constraints are coming, and that spells problems. How does one make money in the natural gas market these days when the price of gas is at historic lows? One way is if an investor was fortunate enough to bet the price would go down. Those folks made money. The other way is to…invest in drillers? Yep. Even though low prices hurt drillers, investors still like the looks of what is on the horizon, especially for companies operating in the Marcellus/Utica. Example: The stock price for Range Resources and EQT is up over 30% each this year so far.

How does one make money in the natural gas market these days when the price of gas is at historic lows? One way is if an investor was fortunate enough to bet the price would go down. Those folks made money. The other way is to…invest in drillers? Yep. Even though low prices hurt drillers, investors still like the looks of what is on the horizon, especially for companies operating in the Marcellus/Utica. Example: The stock price for Range Resources and EQT is up over 30% each this year so far. Here’s a little known factoid that will be useful for anyone wondering what the price of NGLs (natural gas liquids) will bring in a given market at a given time. The U.S. Energy Information Administration (EIA), our favorite government agency, points out NGLs almost always fetch prices that are “range-bound” between the price of oil on the high end, and the price of natural gas on the low end. Natural gasoline (an NGL) tracks closest the high end and the price of crude oil, while ethane is at the bottom of list closest to the price of methane.

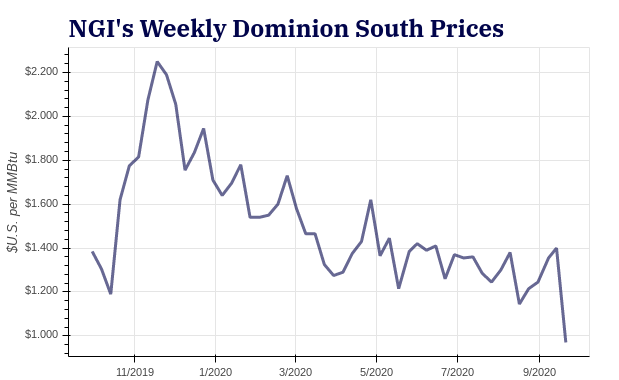

Here’s a little known factoid that will be useful for anyone wondering what the price of NGLs (natural gas liquids) will bring in a given market at a given time. The U.S. Energy Information Administration (EIA), our favorite government agency, points out NGLs almost always fetch prices that are “range-bound” between the price of oil on the high end, and the price of natural gas on the low end. Natural gasoline (an NGL) tracks closest the high end and the price of crude oil, while ethane is at the bottom of list closest to the price of methane. The price of natural gas and what it fetches (by geography) is always a top concern for both drillers and landowners. Recently the price of natgas nationwide has been trading at a 25-year low (see

The price of natural gas and what it fetches (by geography) is always a top concern for both drillers and landowners. Recently the price of natgas nationwide has been trading at a 25-year low (see  Our favorite government agency, the U.S. Energy Information Administration (EIA), issued its monthly Short-Term Energy Outlook (STEO) yesterday. We’re interested mainly in the natural gas numbers. The expert number crunchers at EIA predict the price of Henry Hub traded gas will average $1.93 for all of 2020 (although EIA predicts the price will rise in Q420 to $2.46). The report also says U.S. LNG exports are taking a nosedive this summer. From June through August at least 110 LNG cargoes have been canceled–meaning a decrease in 75% of our LNG exports. That will have a big impact on gas drillers.

Our favorite government agency, the U.S. Energy Information Administration (EIA), issued its monthly Short-Term Energy Outlook (STEO) yesterday. We’re interested mainly in the natural gas numbers. The expert number crunchers at EIA predict the price of Henry Hub traded gas will average $1.93 for all of 2020 (although EIA predicts the price will rise in Q420 to $2.46). The report also says U.S. LNG exports are taking a nosedive this summer. From June through August at least 110 LNG cargoes have been canceled–meaning a decrease in 75% of our LNG exports. That will have a big impact on gas drillers. Reuters is reporting natural gas prices “collapsed” over 7% and hit a “near 25-year low” yesterday. The article says demand destruction from the coronavirus and worldwide shutdowns, along with an excess supply in storage caverns which are “expected to be full by the end of the summer season,” is the reason. Gas in storage is currently 18% above the 5-year average. The July futures NYMEX natural gas price contract, which expires today, was down -9.5% yesterday to $1.44/MMBtu. The August contract closed down -7.9% to $1.53/MMBtu.

Reuters is reporting natural gas prices “collapsed” over 7% and hit a “near 25-year low” yesterday. The article says demand destruction from the coronavirus and worldwide shutdowns, along with an excess supply in storage caverns which are “expected to be full by the end of the summer season,” is the reason. Gas in storage is currently 18% above the 5-year average. The July futures NYMEX natural gas price contract, which expires today, was down -9.5% yesterday to $1.44/MMBtu. The August contract closed down -7.9% to $1.53/MMBtu. The received wisdom has been that with the oil markets getting whacked by the Saudis, the Russians, and the virus, and with new drilling scaled back and oil wells in the Permian, Bakken, Eagle Ford and other oil plays being shut-in, far less “associated gas” would be produced, leading to tighter natgas supplies further leading to higher prices for natgas (benefitting the Marcellus/Utica). But the price of natgas has remained at a 25-year low. What the heck is going on?

The received wisdom has been that with the oil markets getting whacked by the Saudis, the Russians, and the virus, and with new drilling scaled back and oil wells in the Permian, Bakken, Eagle Ford and other oil plays being shut-in, far less “associated gas” would be produced, leading to tighter natgas supplies further leading to higher prices for natgas (benefitting the Marcellus/Utica). But the price of natgas has remained at a 25-year low. What the heck is going on?

With EQT shutting in one-third of its production, Cabot shutting in some of its production, and today’s news that CNX has shut in production (see CNX Update: Shut-in 375 MMcf/d, Central PA Utica the Future), the cumulative effect of those three (plus other M-U drillers) is that our region now produces at least 2 billion cubic feet per day (Bcf/d) less of natgas than it did just a few months ago. That decrease is helping to “balance” gas flows and help prices to not drop further than they already have.

With EQT shutting in one-third of its production, Cabot shutting in some of its production, and today’s news that CNX has shut in production (see CNX Update: Shut-in 375 MMcf/d, Central PA Utica the Future), the cumulative effect of those three (plus other M-U drillers) is that our region now produces at least 2 billion cubic feet per day (Bcf/d) less of natgas than it did just a few months ago. That decrease is helping to “balance” gas flows and help prices to not drop further than they already have. We spotted an article by ICIS (Independent Commodity Intelligence Services) about ethylene contracts in May increasing in price after a six-month-long decline. How does that potentially impact drillers in the Marcellus/Utica? We’ll tell you…

We spotted an article by ICIS (Independent Commodity Intelligence Services) about ethylene contracts in May increasing in price after a six-month-long decline. How does that potentially impact drillers in the Marcellus/Utica? We’ll tell you… Feedgas, which is the gas that flows to LNG export facilities, hit the lowest levels it has seen since last October according to the U.S. Energy Information Administration. As we pointed out two weeks ago, natural gas prices are staying low because worldwide demand and prices for LNG is currently low (see

Feedgas, which is the gas that flows to LNG export facilities, hit the lowest levels it has seen since last October according to the U.S. Energy Information Administration. As we pointed out two weeks ago, natural gas prices are staying low because worldwide demand and prices for LNG is currently low (see