CNG/LNG | Duke Energy | Electrical Generation | Energy Services | Industrywide Issues | North Carolina

Duke Picks Davie County for 2 Gas Plants, Davidson for LNG Facility

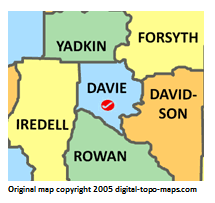

In January, MDN broke the news that Duke Energy was eyeing a 1,360-megawatt (MW) gas-fired power plant on 1,600 acres in Davidson County, North Carolina (see Duke Energy Considers 1,360-MW Gas Plant for Davidson County, NC). In April, we updated it: Duke actually wanted two such plants, and had a second candidate site directly across the Yadkin River in Davie County (see Duke Energy Considers 2 New Large Gas-Fired Power Plants in NC). Duke said back then that a final decision wouldn’t come until late 2026 or early 2027. Surprise! The decision landed today, and Duke didn’t pick one site over the other. It’s using both. Read More “Duke Picks Davie County for 2 Gas Plants, Davidson for LNG Facility”

In January, MDN broke the news that Duke Energy was eyeing a 1,360-megawatt (MW) gas-fired power plant on 1,600 acres in Davidson County, North Carolina (see Duke Energy Considers 1,360-MW Gas Plant for Davidson County, NC). In April, we updated it: Duke actually wanted two such plants, and had a second candidate site directly across the Yadkin River in Davie County (see Duke Energy Considers 2 New Large Gas-Fired Power Plants in NC). Duke said back then that a final decision wouldn’t come until late 2026 or early 2027. Surprise! The decision landed today, and Duke didn’t pick one site over the other. It’s using both. Read More “Duke Picks Davie County for 2 Gas Plants, Davidson for LNG Facility”

A new S&P Global Energy study (full copy below) projects U.S. LNG will become the nation’s second-largest net export industry by 2031, trailing only civilian aircraft and parts. Feedgas demand for exports is expected to double to 36 Bcf/d within five years — 25% above the prior base case — as the U.S. surpasses a one-third share of the global market. Through 2040, LNG should support 555,000 jobs annually, add $1.4 trillion to GDP, and generate $2.9 trillion in business revenues, $206 billion in taxes, and $630 billion in labor income, on more than $1 trillion of supply-chain investment. Household gas costs rise just 1.6% from 2026-2031, and new Northeast pipeline capacity could cut peak winter prices more than 20%.

A new S&P Global Energy study (full copy below) projects U.S. LNG will become the nation’s second-largest net export industry by 2031, trailing only civilian aircraft and parts. Feedgas demand for exports is expected to double to 36 Bcf/d within five years — 25% above the prior base case — as the U.S. surpasses a one-third share of the global market. Through 2040, LNG should support 555,000 jobs annually, add $1.4 trillion to GDP, and generate $2.9 trillion in business revenues, $206 billion in taxes, and $630 billion in labor income, on more than $1 trillion of supply-chain investment. Household gas costs rise just 1.6% from 2026-2031, and new Northeast pipeline capacity could cut peak winter prices more than 20%.

The International Gas Union’s 2026 World LNG Report shows global LNG trade hit a record high of 436.98 million tonnes (Mt) in 2025, up 6.3%—the strongest growth since 2022—driven by a 25.3 Mt surge in North American exports and Europe’s return as the key balancing market. Canada and Mauritania–Senegal became first-time exporters. Investment in new supply reached a six-year high. The LNG fleet grew 8.4% to 804 vessels, with 301 newbuilds on order, keeping freight rates depressed, while bunkering infrastructure expanded. Despite disruptions from the Gulf conflict that damaged infrastructure and the closure of the Strait of Hormuz, the IGU says LNG’s long-term demand outlook through 2035 remains intact.

The International Gas Union’s 2026 World LNG Report shows global LNG trade hit a record high of 436.98 million tonnes (Mt) in 2025, up 6.3%—the strongest growth since 2022—driven by a 25.3 Mt surge in North American exports and Europe’s return as the key balancing market. Canada and Mauritania–Senegal became first-time exporters. Investment in new supply reached a six-year high. The LNG fleet grew 8.4% to 804 vessels, with 301 newbuilds on order, keeping freight rates depressed, while bunkering infrastructure expanded. Despite disruptions from the Gulf conflict that damaged infrastructure and the closure of the Strait of Hormuz, the IGU says LNG’s long-term demand outlook through 2035 remains intact.  Shell, which dropped “Royal Dutch” from its name after leaving the Netherlands in 2022 due to high taxes and overregulation, is one of the world’s supermajors (oil and gas driller). Shell is also one of (perhaps THE) largest producers and vendors of LNG, or liquefied natural gas, worldwide. The company has just released its tenth annual LNG Outlook 2026 (full copy below), which highlights key trends in 2025 and hauls out the crystal ball to predict where things are heading over the next 25 years. Shell’s annual LNG outlook says shipping disruptions in the Strait of Hormuz from the Iran war—which shut in roughly one-fifth of global monthly LNG supply—could keep 2026 global LNG trade flat if flows normalize within three months, with growth resuming in 2027.

Shell, which dropped “Royal Dutch” from its name after leaving the Netherlands in 2022 due to high taxes and overregulation, is one of the world’s supermajors (oil and gas driller). Shell is also one of (perhaps THE) largest producers and vendors of LNG, or liquefied natural gas, worldwide. The company has just released its tenth annual LNG Outlook 2026 (full copy below), which highlights key trends in 2025 and hauls out the crystal ball to predict where things are heading over the next 25 years. Shell’s annual LNG outlook says shipping disruptions in the Strait of Hormuz from the Iran war—which shut in roughly one-fifth of global monthly LNG supply—could keep 2026 global LNG trade flat if flows normalize within three months, with growth resuming in 2027.  We spotted a press release from Hexagon Agility that the company has secured its largest-ever single order for “Mobile Pipeline” modules from Certarus, valued at about $100 million, with an option for up to $25 million more by 2028. It triggered a “connect the dots” moment for us. Mobile pipelines are another term for virtual pipelines, which is a euphemism for trucking natural gas via CNG (mostly) and sometimes LNG. The Hexagon press release indicates strong new demand for such technology in the AI data center market. No pipeline? No problem! Just truck it in via a virtual pipe instead.

We spotted a press release from Hexagon Agility that the company has secured its largest-ever single order for “Mobile Pipeline” modules from Certarus, valued at about $100 million, with an option for up to $25 million more by 2028. It triggered a “connect the dots” moment for us. Mobile pipelines are another term for virtual pipelines, which is a euphemism for trucking natural gas via CNG (mostly) and sometimes LNG. The Hexagon press release indicates strong new demand for such technology in the AI data center market. No pipeline? No problem! Just truck it in via a virtual pipe instead.  The Golden Pass LNG terminal is a liquefied natural gas (LNG) terminal and regasification facility in Sabine Pass (Port Arthur), Texas. It is among the largest LNG facilities in the world. It can accommodate up to 15.6 million metric tons (MT) of LNG per year, the equivalent of approximately 2 billion cubic feet of natural gas per day (Bcf/d). In April, Golden Pass exported its first LNG cargo (see

The Golden Pass LNG terminal is a liquefied natural gas (LNG) terminal and regasification facility in Sabine Pass (Port Arthur), Texas. It is among the largest LNG facilities in the world. It can accommodate up to 15.6 million metric tons (MT) of LNG per year, the equivalent of approximately 2 billion cubic feet of natural gas per day (Bcf/d). In April, Golden Pass exported its first LNG cargo (see  Freeport LNG has become something of a punchline for its frequent outages. Except it’s no laughing matter. Outages at Freeport have happened so frequently that we’ve lost count (

Freeport LNG has become something of a punchline for its frequent outages. Except it’s no laughing matter. Outages at Freeport have happened so frequently that we’ve lost count ( Sempra Infrastructure announced that its Port Arthur Pipeline Louisiana Connector has entered service, marking progress on U.S. energy infrastructure aimed at supplying global natural gas markets. CEO Justin Bird said the project was completed ahead of schedule and under budget. The pipeline will transport up to 2 billion cubic feet per day (Bcf/d) of U.S. natural gas, including Marcellus/Utica gas, to Port Arthur LNG Phase 1, which is now under construction with a nameplate capacity of about 13 million tonnes per annum (MTPA). The project links with the Gillis Hub Pipeline and the LA Storage facility under construction. It includes 72 miles of 42-inch pipeline and a compressor station.

Sempra Infrastructure announced that its Port Arthur Pipeline Louisiana Connector has entered service, marking progress on U.S. energy infrastructure aimed at supplying global natural gas markets. CEO Justin Bird said the project was completed ahead of schedule and under budget. The pipeline will transport up to 2 billion cubic feet per day (Bcf/d) of U.S. natural gas, including Marcellus/Utica gas, to Port Arthur LNG Phase 1, which is now under construction with a nameplate capacity of about 13 million tonnes per annum (MTPA). The project links with the Gillis Hub Pipeline and the LA Storage facility under construction. It includes 72 miles of 42-inch pipeline and a compressor station.  On March 18, President Trump issued a 60-day waiver pausing the enforcement of the Jones Act (see

On March 18, President Trump issued a 60-day waiver pausing the enforcement of the Jones Act (see  The Appalachian Basin, spanning Pennsylvania, West Virginia, and Ohio, has become America’s premier natural gas province, producing over 35 billion cubic feet daily (Bcf/d) in 2024. Driven by hydraulic fracturing in the Marcellus and Utica shales, private mineral rights, and low breakeven costs below $2 per MMBtu, the basin has reshaped *global* energy markets. How? Infrastructure constraints (lack of pipelines) and Mid-Atlantic political opposition prevent local LNG export terminal development. Even so, Marcellus/Utica gas underwrites domestic power markets, fuels digital infrastructure, and indirectly propelled the United States to become the world’s leading LNG superpower by displacing Gulf Coast gas for export liquefaction.

The Appalachian Basin, spanning Pennsylvania, West Virginia, and Ohio, has become America’s premier natural gas province, producing over 35 billion cubic feet daily (Bcf/d) in 2024. Driven by hydraulic fracturing in the Marcellus and Utica shales, private mineral rights, and low breakeven costs below $2 per MMBtu, the basin has reshaped *global* energy markets. How? Infrastructure constraints (lack of pipelines) and Mid-Atlantic political opposition prevent local LNG export terminal development. Even so, Marcellus/Utica gas underwrites domestic power markets, fuels digital infrastructure, and indirectly propelled the United States to become the world’s leading LNG superpower by displacing Gulf Coast gas for export liquefaction.  On March 18, President Trump issued a 60-day waiver pausing the enforcement of the Jones Act (see

On March 18, President Trump issued a 60-day waiver pausing the enforcement of the Jones Act (see