Antero Resources | Ascent Resources | CNX Resources | Commodity Price | Devon Energy | Energy Companies | EQT Corp | Expand Energy | Gulfport Energy | Industrywide Issues | Range Resources Corp | Seneca Resources

Will Higher NatGas Demand and New Pipes Spur More M-U Production?

Despite rising Northeast gas demand from retiring coal plants and new data centers, plus added Appalachian pipeline capacity, production growth isn’t guaranteed—operators prioritize capital discipline, debt reduction, and shareholder returns over volume. Appalachia has held flat at roughly 33-36 Bcf/d since 2020. Can anything tempt Marcellus/Utica drillers to drill and produce more than they are now? According to RBN Energy, sustained Henry Hub prices above $4/MMBtu (versus the current $3.50-$3.60 long-dated curve) and better takeaway infrastructure could be enough of a temptation. Read More “Will Higher NatGas Demand and New Pipes Spur More M-U Production?”

Despite rising Northeast gas demand from retiring coal plants and new data centers, plus added Appalachian pipeline capacity, production growth isn’t guaranteed—operators prioritize capital discipline, debt reduction, and shareholder returns over volume. Appalachia has held flat at roughly 33-36 Bcf/d since 2020. Can anything tempt Marcellus/Utica drillers to drill and produce more than they are now? According to RBN Energy, sustained Henry Hub prices above $4/MMBtu (versus the current $3.50-$3.60 long-dated curve) and better takeaway infrastructure could be enough of a temptation. Read More “Will Higher NatGas Demand and New Pipes Spur More M-U Production?”

The U.S. Energy Information Administration (EIA) issued its latest monthly Short-Term Energy Outlook (STEO) yesterday. Using the official EIA dartboard, the STEO is the agency’s monthly best estimate of where energy prices and production will go over the next 12 months. There was a revision to the agency’s prediction about the spot price (at the Henry Hub) for natural gas in 2026 and 2027. Last month, the EIA predicted 2026 would end up with an average HH price of $3.60/MMBtu and 2027 would see an average of $3.46/MMBtu. Yesterday, the EIA revised both numbers up by a few pennies. The agency sees an average price of $3.67 this year, up seven cents from last month, and $3.49 in 2027, up three pennies.

The U.S. Energy Information Administration (EIA) issued its latest monthly Short-Term Energy Outlook (STEO) yesterday. Using the official EIA dartboard, the STEO is the agency’s monthly best estimate of where energy prices and production will go over the next 12 months. There was a revision to the agency’s prediction about the spot price (at the Henry Hub) for natural gas in 2026 and 2027. Last month, the EIA predicted 2026 would end up with an average HH price of $3.60/MMBtu and 2027 would see an average of $3.46/MMBtu. Yesterday, the EIA revised both numbers up by a few pennies. The agency sees an average price of $3.67 this year, up seven cents from last month, and $3.49 in 2027, up three pennies.  Global research firm Wood Mackenzie warns that a decade of cheap U.S. natural gas is ending, with Henry Hub prices—historically stuck between $2 and $4 per MMBtu—expected to approach $5 by 2035. The shift is driven by surging demand from LNG exports and AI data centers. U.S. LNG exports jumped from 0.5 Bcf/d in 2016 to 15.0 Bcf/d in 2025, with capacity expected to nearly double by 2031. Meanwhile, power-sector demand could require an additional 17 Bcf/d by the mid-2030s. Supply-side tailwinds—prime drilling acreage, cheap associated gas, and annual productivity gains—have largely run their course. WoodMac says $5 gas remains globally competitive.

Global research firm Wood Mackenzie warns that a decade of cheap U.S. natural gas is ending, with Henry Hub prices—historically stuck between $2 and $4 per MMBtu—expected to approach $5 by 2035. The shift is driven by surging demand from LNG exports and AI data centers. U.S. LNG exports jumped from 0.5 Bcf/d in 2016 to 15.0 Bcf/d in 2025, with capacity expected to nearly double by 2031. Meanwhile, power-sector demand could require an additional 17 Bcf/d by the mid-2030s. Supply-side tailwinds—prime drilling acreage, cheap associated gas, and annual productivity gains—have largely run their course. WoodMac says $5 gas remains globally competitive.  The U.S. Energy Information Administration (EIA) issued its latest monthly Short-Term Energy Outlook (STEO) on Tuesday. Using the official EIA dartboard, the STEO is the agency’s monthly best estimate of where energy prices and production will go over the next 12 months. There was a revision to the agency’s prediction about the spot price (at the Henry Hub) for natural gas in 2026 and 2027. Last month, the EIA predicted 2026 would end up with an average HH price of $3.50/MMBtu and 2027 would see an average of $3.18/MMBtu. On Tuesday, the EIA revised both numbers up. The agency sees an average price of $3.60 this year, up a dime from last month, and $3.46 in 2027, up a robust 28 cents.

The U.S. Energy Information Administration (EIA) issued its latest monthly Short-Term Energy Outlook (STEO) on Tuesday. Using the official EIA dartboard, the STEO is the agency’s monthly best estimate of where energy prices and production will go over the next 12 months. There was a revision to the agency’s prediction about the spot price (at the Henry Hub) for natural gas in 2026 and 2027. Last month, the EIA predicted 2026 would end up with an average HH price of $3.50/MMBtu and 2027 would see an average of $3.18/MMBtu. On Tuesday, the EIA revised both numbers up. The agency sees an average price of $3.60 this year, up a dime from last month, and $3.46 in 2027, up a robust 28 cents.  Here’s a story that may, at first glance, seem to have nothing to do with the Marcellus/Utica. Au contraire! The story of what’s happening with Permian drillers has a great deal to do with the M-U region. Although MDN frequently refers to the Haynesville Shale as the #1 competitor to the M-U because both plays target natural gas as the primary hydrocarbon, would it surprise you to learn that the Permian basin is the #2 producer of natural gas behind the M-U? And it’s catching up. Permian Basin drillers are experiencing starkly contrasting fortunes, reaping historic profits from war-driven oil price rallies while facing negative regional natural gas prices due to severe pipeline bottlenecks. To curb financial losses from associated gas, major producers like Permian Resources and Devon Energy are shutting in wells, while others resort to flaring to maintain more profitable crude production.

Here’s a story that may, at first glance, seem to have nothing to do with the Marcellus/Utica. Au contraire! The story of what’s happening with Permian drillers has a great deal to do with the M-U region. Although MDN frequently refers to the Haynesville Shale as the #1 competitor to the M-U because both plays target natural gas as the primary hydrocarbon, would it surprise you to learn that the Permian basin is the #2 producer of natural gas behind the M-U? And it’s catching up. Permian Basin drillers are experiencing starkly contrasting fortunes, reaping historic profits from war-driven oil price rallies while facing negative regional natural gas prices due to severe pipeline bottlenecks. To curb financial losses from associated gas, major producers like Permian Resources and Devon Energy are shutting in wells, while others resort to flaring to maintain more profitable crude production.

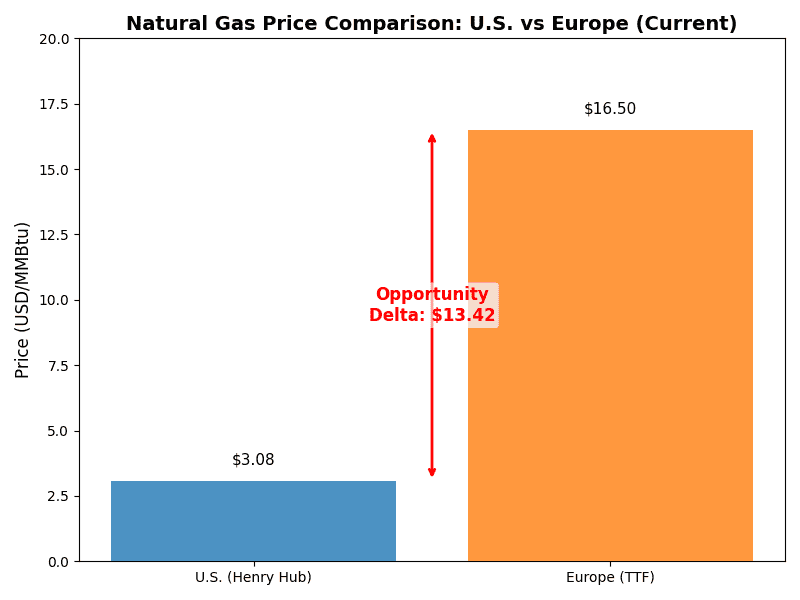

Following the February 28 closure of the Strait of Hormuz, global and U.S. natural gas prices have sharply diverged. The shutdown halted roughly 20% of global LNG supplies, primarily from Qatar, forcing Asian and European buyers to scramble for replacement cargoes. Consequently, European TTF and Asian JKM benchmark prices surged 35% ($14.80/MMBtu) and 51% ($16.02/MMBtu), respectively. In stark contrast, U.S. Henry Hub prices fell 9%. Because U.S. LNG export terminals are already operating at near-maximum capacity, producers cannot significantly increase exports to capture these high global prices. This leaves ample gas domestically, insulating the U.S. market from international price volatility.

Following the February 28 closure of the Strait of Hormuz, global and U.S. natural gas prices have sharply diverged. The shutdown halted roughly 20% of global LNG supplies, primarily from Qatar, forcing Asian and European buyers to scramble for replacement cargoes. Consequently, European TTF and Asian JKM benchmark prices surged 35% ($14.80/MMBtu) and 51% ($16.02/MMBtu), respectively. In stark contrast, U.S. Henry Hub prices fell 9%. Because U.S. LNG export terminals are already operating at near-maximum capacity, producers cannot significantly increase exports to capture these high global prices. This leaves ample gas domestically, insulating the U.S. market from international price volatility.

In January 2026, New England experienced record-high natural gas prices triggered by an intense cold snap. On January 27, wholesale electricity costs reached $441.8/MWh, a significant jump from the previous January’s average of $135.08/MWh. The problem is not enough natural gas pipelines. But that’s not what the dunderheads who run the blue states of New England believe. They think natgas is the problem and that more unreliable renewables are the solution. You can’t fix stupid, but you can vote it out of office.

In January 2026, New England experienced record-high natural gas prices triggered by an intense cold snap. On January 27, wholesale electricity costs reached $441.8/MWh, a significant jump from the previous January’s average of $135.08/MWh. The problem is not enough natural gas pipelines. But that’s not what the dunderheads who run the blue states of New England believe. They think natgas is the problem and that more unreliable renewables are the solution. You can’t fix stupid, but you can vote it out of office.  Hedging is the practice of locking in a price now to sell gas you will produce in the future. We’ve written a fair bit about hedging (

Hedging is the practice of locking in a price now to sell gas you will produce in the future. We’ve written a fair bit about hedging (