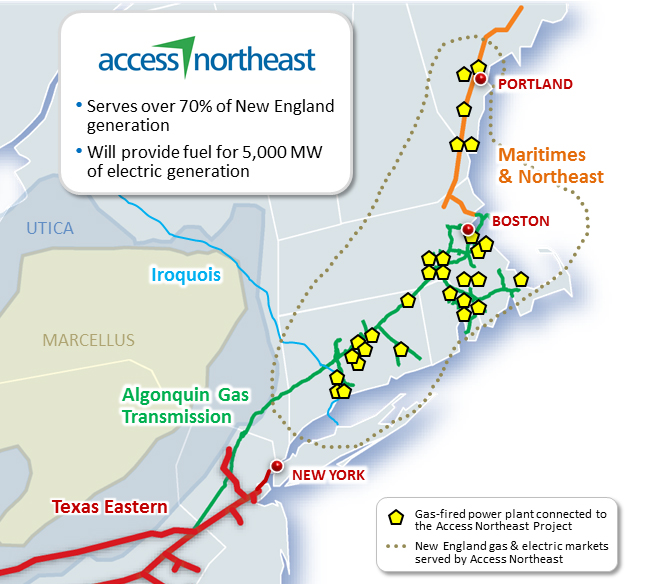

Spectra Energy 2Q16 – Access Northeast “Advancing Toward Execution”

It sure pays to be in the pipeline business. One of the biggest pipeline (i.e. midstream) companies in the U.S. is Spectra Energy. Spectra has a number of existing and planned pipelines in the Marcellus/Utica region. Yesterday Spectra released their second quarter 2016 update, reporting a net income of $305 million for the quarter. Spectra provided a handy list of the ~$6 billion in expansion projects they have under way. One of those projects is the Access Northeast project–representing half of that $6 billion. Access Northeast is the surviving winner of a contest between Spectra Energy and Kinder Morgan to pipe Marcellus and Utica Shale gas to New England and Canada–the “last man standing” when Kinder and their Northeast Energy Direct project bowed out of the race (see NED is Dead – Kinder Morgan Suspends $3.3B New England Pipeline). With respect to Spectra and their Access Northeast project, Spectra CEO Greg Ebel had said yesterday during an earnings conference call that Access Northeast is “advancing towards execution this year” after recently achieving a “number of noteworthy milestones.” That is indeed good news! Here’s yesterday’s 2Q16 update from Spectra, along with an excerpt about Access Northeast from the earnings call…

Read More “Spectra Energy 2Q16 – Access Northeast “Advancing Toward Execution””

MDN felt that the big news today was word from Spectra Energy that their Access Northeast pipeline project is making excellent progress (see Spectra Energy 2Q16 – Access Northeast “Advancing Toward Execution”). However, a bit of news coming from Spectra disclosed on yesterday’s earnings call comes in at a close second. You may recall there was an explosion and fire in Spectra Energy’s Texas Eastern Transmission’s “Delmont Line 27” pipeline in May (see

MDN felt that the big news today was word from Spectra Energy that their Access Northeast pipeline project is making excellent progress (see Spectra Energy 2Q16 – Access Northeast “Advancing Toward Execution”). However, a bit of news coming from Spectra disclosed on yesterday’s earnings call comes in at a close second. You may recall there was an explosion and fire in Spectra Energy’s Texas Eastern Transmission’s “Delmont Line 27” pipeline in May (see  Score an important victory against the forces of darkness. The radical leftist PA-based group Community Environmental Legal Defense Fund (CELDF) does its best to trick townships into passing illegal bans on fracking and injection wells. In 2013 the CELDF fooled Highland Township in Elk County, PA into passing a ban on wastewater injection wells. They also tricked Grant Township in Indiana County, PA to do the same thing. Both towns are in court defending their illegal actions. One of the idiotic legal tactics used by the CELDF in both cases is to claim that an ecosystem is a “person” under the law–a person who can file to join the town’s lawsuit in an effort to protect itself (see

Score an important victory against the forces of darkness. The radical leftist PA-based group Community Environmental Legal Defense Fund (CELDF) does its best to trick townships into passing illegal bans on fracking and injection wells. In 2013 the CELDF fooled Highland Township in Elk County, PA into passing a ban on wastewater injection wells. They also tricked Grant Township in Indiana County, PA to do the same thing. Both towns are in court defending their illegal actions. One of the idiotic legal tactics used by the CELDF in both cases is to claim that an ecosystem is a “person” under the law–a person who can file to join the town’s lawsuit in an effort to protect itself (see  In May the federal Environmental Protection Agency (EPA) once again far overstepped its charter by seizing power that doesn’t belong to it. They issued new methane rules in a back-door way to try and regulate the oil and gas industry (see

In May the federal Environmental Protection Agency (EPA) once again far overstepped its charter by seizing power that doesn’t belong to it. They issued new methane rules in a back-door way to try and regulate the oil and gas industry (see  On Tuesday MDN brought you what we thought was the very first Annual Oil and Gas Annual Report from the Pennsylvania Dept. of Environmental Protection (see

On Tuesday MDN brought you what we thought was the very first Annual Oil and Gas Annual Report from the Pennsylvania Dept. of Environmental Protection (see  MDN spotted what we thought was an interesting article on the Seeking Alpha investors website about the existing pipeline bottleneck in Northeastern PA and what can be done about getting all of that gas to market. Pipeline delays out of NEPA, including the delayed Constitution Pipeline and projects currently underway but taking a long time, like the Atlantic Sunrise, are forcing producers like Cabot Oil & Gas, Southwestern Energy and Chesapeake Energy to look for other ways to move their abundant supplies of natgas out of the region. Eastbound routes out of NEPA are full, but westbound routes *may* be a possible solution–at least in the short-to-medium term. National Fuel Gas’s pipeline system has expanded recently to allow more gas to flow west. NFG has additional projects in the coming years to build on that capacity. Is it time to Go West, Young Molecule?…

MDN spotted what we thought was an interesting article on the Seeking Alpha investors website about the existing pipeline bottleneck in Northeastern PA and what can be done about getting all of that gas to market. Pipeline delays out of NEPA, including the delayed Constitution Pipeline and projects currently underway but taking a long time, like the Atlantic Sunrise, are forcing producers like Cabot Oil & Gas, Southwestern Energy and Chesapeake Energy to look for other ways to move their abundant supplies of natgas out of the region. Eastbound routes out of NEPA are full, but westbound routes *may* be a possible solution–at least in the short-to-medium term. National Fuel Gas’s pipeline system has expanded recently to allow more gas to flow west. NFG has additional projects in the coming years to build on that capacity. Is it time to Go West, Young Molecule?… Rice Energy, a young company headed by relatively young leaders (the Rice boys), continues to impress with their latest quarterly update, for 2Q16. Net production for Rice hit a record 758 million cubic feet equivalent per day (MMcfe/d), which is a 43% increase over 2Q15 and a 12% increase over 1Q16. As CEO Dan Rice said, “We had a remarkable quarter, marked by several notable achievements, including record-low development costs and lease operating expenses, record-high production and midstream throughput volumes, and we turned to sales a company-record 18 operated wells in April.” Rice continues to focus completely on the Marcellus and Utica region, a “pure play” company. Because they’ve lowered costs, Rice is adding another $65 million to their Utica drilling budget in 2016. Cool. About the only bad news from yesterday’s quarterly update is that the company lost $138.7 million in 2Q16, versus losing $63.5 million in 2Q15. But keep an eye out. The Rice boys are bound to turn the financials around. Here’s the update, with details on what Rice accomplished in both the Marcellus and Utica in 2Q16…

Rice Energy, a young company headed by relatively young leaders (the Rice boys), continues to impress with their latest quarterly update, for 2Q16. Net production for Rice hit a record 758 million cubic feet equivalent per day (MMcfe/d), which is a 43% increase over 2Q15 and a 12% increase over 1Q16. As CEO Dan Rice said, “We had a remarkable quarter, marked by several notable achievements, including record-low development costs and lease operating expenses, record-high production and midstream throughput volumes, and we turned to sales a company-record 18 operated wells in April.” Rice continues to focus completely on the Marcellus and Utica region, a “pure play” company. Because they’ve lowered costs, Rice is adding another $65 million to their Utica drilling budget in 2016. Cool. About the only bad news from yesterday’s quarterly update is that the company lost $138.7 million in 2Q16, versus losing $63.5 million in 2Q15. But keep an eye out. The Rice boys are bound to turn the financials around. Here’s the update, with details on what Rice accomplished in both the Marcellus and Utica in 2Q16…

We found this story amusing. A group of 40 anti-fossil fuel nutters met at the Towamensing Township fire hall Tuesday night to “hone their arguments and strategies on how to derail or at least delay construction” of the $1.2 billion PennEast Pipeline. Why is that amusing? Because if the media is reporting there were 40 there, that means there were really 20-25. And when you read the story, you get the distinct impression that a very small group of hardened anti-fossil fuelers move these meetings around–it’s the same small group–and that their movement to stop PennEast is dying. Rapidly. Here’s the latest evidence…

We found this story amusing. A group of 40 anti-fossil fuel nutters met at the Towamensing Township fire hall Tuesday night to “hone their arguments and strategies on how to derail or at least delay construction” of the $1.2 billion PennEast Pipeline. Why is that amusing? Because if the media is reporting there were 40 there, that means there were really 20-25. And when you read the story, you get the distinct impression that a very small group of hardened anti-fossil fuelers move these meetings around–it’s the same small group–and that their movement to stop PennEast is dying. Rapidly. Here’s the latest evidence… The “best of the rest” – stories that caught MDN’s eye that you may be interested in reading. In today’s lineup: TransCanada chooses growth over fiscal discipline; Kennametal cutting 1K jobs due to drilling slowdown; crude-by-rail volumes dropping; Magellan merging with Tellurian; AEP industrial sales own on restrained shale development; and more!

The “best of the rest” – stories that caught MDN’s eye that you may be interested in reading. In today’s lineup: TransCanada chooses growth over fiscal discipline; Kennametal cutting 1K jobs due to drilling slowdown; crude-by-rail volumes dropping; Magellan merging with Tellurian; AEP industrial sales own on restrained shale development; and more!