Which Natural Gas Markets Will Grow, by Sector, from Now to 2050?

The U.S. Energy Information Administration (EIA) recently issued its Annual Energy Outlook for 2021 (see EIA Annual Energy Outlook 2021: COVID Impact at Least 10 More Yrs). Using the “reference case” (the most likely scenario) from that study, analysts at EIA have taken a close look at the growth in natural gas usage from now until 2050. They found natgas usage in two sectors will grow the most over the next 30 years…

The U.S. Energy Information Administration (EIA) recently issued its Annual Energy Outlook for 2021 (see EIA Annual Energy Outlook 2021: COVID Impact at Least 10 More Yrs). Using the “reference case” (the most likely scenario) from that study, analysts at EIA have taken a close look at the growth in natural gas usage from now until 2050. They found natgas usage in two sectors will grow the most over the next 30 years…

Read More “Which Natural Gas Markets Will Grow, by Sector, from Now to 2050?”

The so-called peak oil theorists have been positively giddy with excitement over predictions about the death of oil. “Just look at how much oil production demand AND supply has decreased since the outbreak of the pandemic. It’s NEVER coming back!” Those are the kinds of things the peakers tell themselves and anyone else who will listen. Mainstream media laps it up and repeats it. But when real researchers delve into the topic of whether or not oil has reached its zenith, the facts tell a far different story.

The so-called peak oil theorists have been positively giddy with excitement over predictions about the death of oil. “Just look at how much oil production demand AND supply has decreased since the outbreak of the pandemic. It’s NEVER coming back!” Those are the kinds of things the peakers tell themselves and anyone else who will listen. Mainstream media laps it up and repeats it. But when real researchers delve into the topic of whether or not oil has reached its zenith, the facts tell a far different story. For the past week or so we’ve spotted stories in the Democrat press (i.e. mainstream news) about a so-called “research report” issued by a front organization for the Heinz Endowments called the Ohio River Valley Institute (ORVI). The ORVI recently released a report that purports to show the fracking miracle in the Marcellus/Utica hasn’t actually created all that many jobs or economic benefits. Here’s the first tip this report is a scam and a sham: The lead researcher from the so-called ORVI doesn’t live in the Ohio River Valley nor anywhere near the M-U, he’s a playwright who lives thousands of miles away on the Left Coast, in Washington State. In other words, the report is fiction.

For the past week or so we’ve spotted stories in the Democrat press (i.e. mainstream news) about a so-called “research report” issued by a front organization for the Heinz Endowments called the Ohio River Valley Institute (ORVI). The ORVI recently released a report that purports to show the fracking miracle in the Marcellus/Utica hasn’t actually created all that many jobs or economic benefits. Here’s the first tip this report is a scam and a sham: The lead researcher from the so-called ORVI doesn’t live in the Ohio River Valley nor anywhere near the M-U, he’s a playwright who lives thousands of miles away on the Left Coast, in Washington State. In other words, the report is fiction.

Over the past several weeks the Enverus U.S. rig count had rocketed skyward, making gains of more than a dozen rigs added each week. Over the past week that torrid pace slowed. In the past seven days, the active rig count added just one new rig to the national total. The Marcellus lost two rigs, one each in the dry gas northeast and wet gas southwest. The Utica gained one rig, for a net loss of -1 in the M-U region (now at 42 active rigs).

Over the past several weeks the Enverus U.S. rig count had rocketed skyward, making gains of more than a dozen rigs added each week. Over the past week that torrid pace slowed. In the past seven days, the active rig count added just one new rig to the national total. The Marcellus lost two rigs, one each in the dry gas northeast and wet gas southwest. The Utica gained one rig, for a net loss of -1 in the M-U region (now at 42 active rigs). Our favorite government agency, the U.S. Energy Information Administration (EIA), is a sub-unit of the Dept. of Energy. The DOE, as you know, is now part of the Evil Empire (aka the Biden Administration). As you also know, old dementia Joe has been bashing away at fossil fuels since he took office, promising to “transition away” from fossil fuels during his tenure of occupying the White House. Yet the EIA is out with a projection that shows “renewables” (includes not just wind and solar but hydro and “other”) will still make up less than half (42%) of electric power production 30 years from now! Fossil fuels (natural gas and coal) will still have a larger share of electric production than renewables 30 years from now. How’s that for a “transition away” from fossil fuels?

Our favorite government agency, the U.S. Energy Information Administration (EIA), is a sub-unit of the Dept. of Energy. The DOE, as you know, is now part of the Evil Empire (aka the Biden Administration). As you also know, old dementia Joe has been bashing away at fossil fuels since he took office, promising to “transition away” from fossil fuels during his tenure of occupying the White House. Yet the EIA is out with a projection that shows “renewables” (includes not just wind and solar but hydro and “other”) will still make up less than half (42%) of electric power production 30 years from now! Fossil fuels (natural gas and coal) will still have a larger share of electric production than renewables 30 years from now. How’s that for a “transition away” from fossil fuels? Yesterday our favorite government agency, the U.S. Energy Information Administration (EIA), released its “Annual Energy Outlook 2021.” One of the main themes of this year’s AEO is the profound impact COVID-19 has had and will continue to have on energy usage worldwide. EIA says it will likely take a decade or more for energy usage to return to the pre-pandemic levels of 2019.

Yesterday our favorite government agency, the U.S. Energy Information Administration (EIA), released its “Annual Energy Outlook 2021.” One of the main themes of this year’s AEO is the profound impact COVID-19 has had and will continue to have on energy usage worldwide. EIA says it will likely take a decade or more for energy usage to return to the pre-pandemic levels of 2019. Did you know that the Appalachia Basin, made up of the Marcellus and Utica Shale, accounted for more than 40% of the natural gas produced in the US in 2020? The M-U averaged 32.19 billion cubic feet per day (Bcf/d) of natural gas production in 2020, and 33.44 Bcf/d in 2019. A new report from GlobalData says the outlook for the Marcellus and Utica plays is closely tied to the demand for LNG exports from the U.S. You might say they’re “joined at the hip.” Unfortunately, most LNG exports happen along the Gulf Coast.

Did you know that the Appalachia Basin, made up of the Marcellus and Utica Shale, accounted for more than 40% of the natural gas produced in the US in 2020? The M-U averaged 32.19 billion cubic feet per day (Bcf/d) of natural gas production in 2020, and 33.44 Bcf/d in 2019. A new report from GlobalData says the outlook for the Marcellus and Utica plays is closely tied to the demand for LNG exports from the U.S. You might say they’re “joined at the hip.” Unfortunately, most LNG exports happen along the Gulf Coast. Yesterday our favorite government agency, the U.S. Energy Information Administration (EIA), published our favorite monthly report, the Drilling Productivity Report (DPR). The latest DPR, which shows estimates for oil and gas production from the seven largest shale plays in the U.S., shows a drop in shale gas production across all plays (including the Marcellus/Utica) coming in February–except for an increase in gas production in the M-U’s primary competitor, the Haynesville.

Yesterday our favorite government agency, the U.S. Energy Information Administration (EIA), published our favorite monthly report, the Drilling Productivity Report (DPR). The latest DPR, which shows estimates for oil and gas production from the seven largest shale plays in the U.S., shows a drop in shale gas production across all plays (including the Marcellus/Utica) coming in February–except for an increase in gas production in the M-U’s primary competitor, the Haynesville. Although we consider the Haynesville Shale play to be the chief competitor to the Marcellus/Utica (because the Haynesville is also a gas play and currently operates more rigs that we do here in the M-U), the Permian is another major competitor. After the M-U, the Permian produces more natural gas (associated gas) than any other play, including the Haynesville. According to the experts at RBN Energy, the Permian is already back to producing as much natural gas as it did prior to the pandemic, and the numbers will only continue to climb.

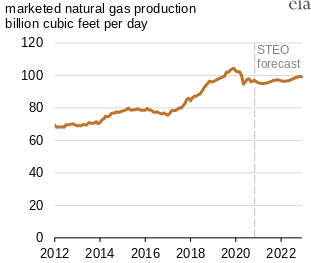

Although we consider the Haynesville Shale play to be the chief competitor to the Marcellus/Utica (because the Haynesville is also a gas play and currently operates more rigs that we do here in the M-U), the Permian is another major competitor. After the M-U, the Permian produces more natural gas (associated gas) than any other play, including the Haynesville. According to the experts at RBN Energy, the Permian is already back to producing as much natural gas as it did prior to the pandemic, and the numbers will only continue to climb. In its January 2021 Short-Term Energy Outlook (STEO) just released, the U.S. Energy Information Administration (EIA) forecasts annual average production of U.S. oil will fall to 11.1 million barrels per day (b/d) in 2021 before rising to 11.5 million b/d in 2022. As for natural gas, EIA says U.S. marketed natural gas production will decline by 2% to an average of 95.9 billion cubic feet per day (Bcf/d) in 2021. Like oil, EIA predicts the fall in natgas production will reverse in 2022 and will rise by 2% to 97.6 Bcf/d.

In its January 2021 Short-Term Energy Outlook (STEO) just released, the U.S. Energy Information Administration (EIA) forecasts annual average production of U.S. oil will fall to 11.1 million barrels per day (b/d) in 2021 before rising to 11.5 million b/d in 2022. As for natural gas, EIA says U.S. marketed natural gas production will decline by 2% to an average of 95.9 billion cubic feet per day (Bcf/d) in 2021. Like oil, EIA predicts the fall in natgas production will reverse in 2022 and will rise by 2% to 97.6 Bcf/d. Researchers at the University of Illinois Chicago have developed a cutting edge catalyst made up of 10 different elements–each of which on its own has the ability to reduce the combustion temperature of methane–plus oxygen. This unique catalyst brings the combustion temperature of methane down by about half, from above 1400 degrees Kelvin down to 600 to 700 degrees Kelvin. What it means is that natural gas can burn cleaner and emit far less carbon dioxide.

Researchers at the University of Illinois Chicago have developed a cutting edge catalyst made up of 10 different elements–each of which on its own has the ability to reduce the combustion temperature of methane–plus oxygen. This unique catalyst brings the combustion temperature of methane down by about half, from above 1400 degrees Kelvin down to 600 to 700 degrees Kelvin. What it means is that natural gas can burn cleaner and emit far less carbon dioxide.