EQT Plans to Make Money with $2/Mcf NatGas Price

For years MDN has observed that Cabot Oil & Gas is one of the few Marcellus/Utica drilling companies that can “spin straw into gold”–meaning it makes money on selling natural gas even when the price of that gas is in the basement (see Marcellus Driller Cabot Oil & Gas: Wall Street’s NatGas “Unicorn”). The new management at EQT aim to turn their company in a spinning-straw-into-gold company too. In a recent interview with the Pittsburgh Business Times, EQT CEO Toby Rice said his strategy for making $500 million in “free cash flow” within two years anticipates the price of natgas to be $2 per thousand cubic feet (Mcf).

For years MDN has observed that Cabot Oil & Gas is one of the few Marcellus/Utica drilling companies that can “spin straw into gold”–meaning it makes money on selling natural gas even when the price of that gas is in the basement (see Marcellus Driller Cabot Oil & Gas: Wall Street’s NatGas “Unicorn”). The new management at EQT aim to turn their company in a spinning-straw-into-gold company too. In a recent interview with the Pittsburgh Business Times, EQT CEO Toby Rice said his strategy for making $500 million in “free cash flow” within two years anticipates the price of natgas to be $2 per thousand cubic feet (Mcf).

Read More “EQT Plans to Make Money with $2/Mcf NatGas Price”

No doubt you’ve noticed the price of natural gas has been relatively low over the past few weeks, dropping from around $2.40 per thousand cubic feet (Mcf) a month ago to now flirting with $2/Mcf. The last time gas prices went below $2/Mcf was in 2016. One of the reasons, believe it or not, that the price has fallen dramatically over the past few days is because of a single LNG export facility–Cheniere Energy’s Sabine Pass facility (which exports some M-U gas).

No doubt you’ve noticed the price of natural gas has been relatively low over the past few weeks, dropping from around $2.40 per thousand cubic feet (Mcf) a month ago to now flirting with $2/Mcf. The last time gas prices went below $2/Mcf was in 2016. One of the reasons, believe it or not, that the price has fallen dramatically over the past few days is because of a single LNG export facility–Cheniere Energy’s Sabine Pass facility (which exports some M-U gas).

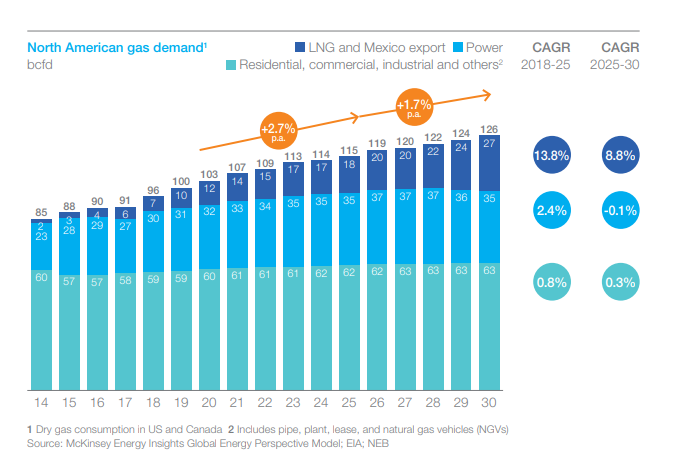

The pipeline situation today in the Marcellus/Utica region is far different than it was just a year or two ago. Not long ago lack of pipelines meant we had an overabundance of natural gas in the region without buyers, driving prices into the basement. Today? It’s all different. Because of new and expanded pipelines coming online over the past couple of years, producers (i.e. drillers) today have options on where to send their natural gas–fetching far better prices in new markets. In fact, according to the analysts at RBN Energy, “The spate of pipeline expansions and additions in the past two years have not only caught up to production but capacity now far outpaces it.” That’s a big switcheroo.

The pipeline situation today in the Marcellus/Utica region is far different than it was just a year or two ago. Not long ago lack of pipelines meant we had an overabundance of natural gas in the region without buyers, driving prices into the basement. Today? It’s all different. Because of new and expanded pipelines coming online over the past couple of years, producers (i.e. drillers) today have options on where to send their natural gas–fetching far better prices in new markets. In fact, according to the analysts at RBN Energy, “The spate of pipeline expansions and additions in the past two years have not only caught up to production but capacity now far outpaces it.” That’s a big switcheroo. The Natural Gas Supply Association (NGSA) yesterday released its 2019 Summer Outlook for Natural Gas report (summary below). It’s not much different than the Winter Outlook was (see

The Natural Gas Supply Association (NGSA) yesterday released its 2019 Summer Outlook for Natural Gas report (summary below). It’s not much different than the Winter Outlook was (see

This is nuts! This is insane! Because of overproduction, lack of pipelines, and an existing pipeline down for maintenance, natural gas sellers at the Waha natural gas trading hub (in West Texas) are actually paying buyers to take the gas off their hands–up to an amazing $5 per thousand cubic feet!!!!

This is nuts! This is insane! Because of overproduction, lack of pipelines, and an existing pipeline down for maintenance, natural gas sellers at the Waha natural gas trading hub (in West Texas) are actually paying buyers to take the gas off their hands–up to an amazing $5 per thousand cubic feet!!!! Reuters is reporting that the price of natural gas selling at the Waha Hub in the Permian Basin (West Texas) averaged just $0.12 (12 cents) per thousand cubic feet (Mcf) yesterday, a new record low. But wait! MDN reported last November the price at Waha had hit minus 1 cent/Mcf–people paying someone else to take their gas (see

Reuters is reporting that the price of natural gas selling at the Waha Hub in the Permian Basin (West Texas) averaged just $0.12 (12 cents) per thousand cubic feet (Mcf) yesterday, a new record low. But wait! MDN reported last November the price at Waha had hit minus 1 cent/Mcf–people paying someone else to take their gas (see  The folks at Argus Media have done an analysis of the number of shale well permits issued in Pennsylvania for January 2019. The numbers show the number of new permits issued during January were up 72% from the number issued in December 2018, but down 11% from the number of permits issued in January 2018, one year earlier. Can we divine anything from this mixed bag of numbers?

The folks at Argus Media have done an analysis of the number of shale well permits issued in Pennsylvania for January 2019. The numbers show the number of new permits issued during January were up 72% from the number issued in December 2018, but down 11% from the number of permits issued in January 2018, one year earlier. Can we divine anything from this mixed bag of numbers? Sorry to burst your bubble, all you gas bulls who believe low storage numbers + weather (hot or cold) = high natgas prices for the long term.

Sorry to burst your bubble, all you gas bulls who believe low storage numbers + weather (hot or cold) = high natgas prices for the long term. Antero Resources, one of the biggest drillers in the Marcellus/Utica, is also one of the best hedging companies in the business. They routinely lock in prices for their gas up to a year (or more) in advance, to ensure they make a tidy profit. And Antero averages higher prices for their gas sales than just about any other Marcellus/Utica producer. This morning Antero issued an update on their latest hedging moves, which is always interesting. But that’s not what caught our eye. They also issued a fourth quarter update. No, not for the entire fourth quarter as we still have a few weeks left in 4Q and the full, official 4Q update won’t come along until maybe the end of January. But in this interim 4Q update, we spotted the news that because of the addition of the Rover Pipeline, Antero now sells a full 30% (up from 16%) of their natural gas production to Midwest markets–markets that pay, on average, more for gas than elsewhere.

Antero Resources, one of the biggest drillers in the Marcellus/Utica, is also one of the best hedging companies in the business. They routinely lock in prices for their gas up to a year (or more) in advance, to ensure they make a tidy profit. And Antero averages higher prices for their gas sales than just about any other Marcellus/Utica producer. This morning Antero issued an update on their latest hedging moves, which is always interesting. But that’s not what caught our eye. They also issued a fourth quarter update. No, not for the entire fourth quarter as we still have a few weeks left in 4Q and the full, official 4Q update won’t come along until maybe the end of January. But in this interim 4Q update, we spotted the news that because of the addition of the Rover Pipeline, Antero now sells a full 30% (up from 16%) of their natural gas production to Midwest markets–markets that pay, on average, more for gas than elsewhere. MDN has run a number of stories on the recent wild fluctuations in the price of natural gas. As we always explain, there is no one “price” of natgas for everyone–but there is the Henry Hub price, which is used for trading futures contracts (NYMEX). That price is watched like a hawk by everyone who trades natural gas. A casual observer of the market might think, based on media coverage, that the swings in the NYMEX price mean something bad. Negative. “The price I’ll pay this winter will go high, and it will stay high, and the shale “revolution” was always just a mirage and this proves it!” Whew. Take a chill pill. The chief economist for the American Petroleum Institute recently penned what we call a natgas price explainer, looking at the recent spikes in the price, providing context for understanding that the price we pay for gas is still, on average, at historic lows. And no, the sky is not falling.

MDN has run a number of stories on the recent wild fluctuations in the price of natural gas. As we always explain, there is no one “price” of natgas for everyone–but there is the Henry Hub price, which is used for trading futures contracts (NYMEX). That price is watched like a hawk by everyone who trades natural gas. A casual observer of the market might think, based on media coverage, that the swings in the NYMEX price mean something bad. Negative. “The price I’ll pay this winter will go high, and it will stay high, and the shale “revolution” was always just a mirage and this proves it!” Whew. Take a chill pill. The chief economist for the American Petroleum Institute recently penned what we call a natgas price explainer, looking at the recent spikes in the price, providing context for understanding that the price we pay for gas is still, on average, at historic lows. And no, the sky is not falling. The evidence continues to pour in that the addition of Williams’ Atlantic Sunrise Pipeline, a 200-mile greenfield pipeline from northeastern to southeastern PA where it joins the Transco Pipeline, is having a dramatic and ongoing effect on natural gas prices in northeastern PA. As in, the price drillers get for their gas has doubled. Atlantic Sunrise went online in early October (see

The evidence continues to pour in that the addition of Williams’ Atlantic Sunrise Pipeline, a 200-mile greenfield pipeline from northeastern to southeastern PA where it joins the Transco Pipeline, is having a dramatic and ongoing effect on natural gas prices in northeastern PA. As in, the price drillers get for their gas has doubled. Atlantic Sunrise went online in early October (see  This one will make your head explode. We’ve been warning about this for some time, or rather, RBN Energy has been warning about it (and we’ve brought you their warnings). During a recent three hour period of natural gas trading at the Waha Hub (in West Texas), the price of gas went to negative 1 cent per thousand cubic feet (Mcf). You read that right. Someone was paying someone else to buy the gas from them! Why? Too much “associated gas” being produced in the prolific Permian Basin, and not enough pipelines to carry it to other markets. The Permian is all about oil drilling. Natural gas is a byproduct, to the point it may be worth giving it away for free just to get rid of it so a driller can keep pumping oil. The proliferation of natgas in the region is driving prices into the subbasement.

This one will make your head explode. We’ve been warning about this for some time, or rather, RBN Energy has been warning about it (and we’ve brought you their warnings). During a recent three hour period of natural gas trading at the Waha Hub (in West Texas), the price of gas went to negative 1 cent per thousand cubic feet (Mcf). You read that right. Someone was paying someone else to buy the gas from them! Why? Too much “associated gas” being produced in the prolific Permian Basin, and not enough pipelines to carry it to other markets. The Permian is all about oil drilling. Natural gas is a byproduct, to the point it may be worth giving it away for free just to get rid of it so a driller can keep pumping oil. The proliferation of natgas in the region is driving prices into the subbasement. This is an “I told you so” post. Last Wednesday, just ahead of what was perhaps the coldest temps for Thanksgiving on record in New England, the price of electricity and the price of natural gas both spiked in New England. Most electricity produced in the region is produced by burning natural gas. Natgas was selling for $13.70/Mcf (thousand cubic feet, or million BTUs) last Wednesday. That was up from an average of $4.67/Mcf this year (up almost 300%). The reason for the spike is lack of natural gas, and the reason for lack of natural gas is a lack of pipelines, plain and simple. And this won’t be the last time. New England will get hosed this winter as prices rocket every time there’s a cold snap. We take no pleasure in saying, “Told you so.”

This is an “I told you so” post. Last Wednesday, just ahead of what was perhaps the coldest temps for Thanksgiving on record in New England, the price of electricity and the price of natural gas both spiked in New England. Most electricity produced in the region is produced by burning natural gas. Natgas was selling for $13.70/Mcf (thousand cubic feet, or million BTUs) last Wednesday. That was up from an average of $4.67/Mcf this year (up almost 300%). The reason for the spike is lack of natural gas, and the reason for lack of natural gas is a lack of pipelines, plain and simple. And this won’t be the last time. New England will get hosed this winter as prices rocket every time there’s a cold snap. We take no pleasure in saying, “Told you so.”