Natural Gas Prices in Texas Permian Drop Below Marcellus/Utica

The biggest oil play in the United States is the Permian, located in West Texas and southeastern New Mexico. Two weeks ago MDN warned readers that natural gas in the Permian, which is a byproduct of the oil wells drilled there, is increasingly competing with Marcellus/Utica gas (see “Free” NatGas in Texas Permian Changes Shale Gas Economics in M-U). The coming clash continues to grow. In a Bloomberg article published yesterday, we learn that the price of natgas in the Permian at major trading hubs is now lower than the price for hubs around the Marcellus/Utica, which is truly a first! We also get an ominous prediction from an analyst who watches these things, who said in the next three to four weeks, “natural gas prices in the Permian can go to zero because it’s literally a byproduct.” Free gas! As we pointed out in our previous post on Permian and gas prices, oil drillers can actually pay up to $2.36 per thousand cubic feet to dispose of the natgas coming out of Permian oil wells. That is, they can pay people to take the gas–as a cost of extracting the oil. Roughly one-third of the hydrocarbons coming from Permian wells is natgas. The biggest problem in the Permian for natgas is also the biggest problem in the M-U: lack of pipelines…

The biggest oil play in the United States is the Permian, located in West Texas and southeastern New Mexico. Two weeks ago MDN warned readers that natural gas in the Permian, which is a byproduct of the oil wells drilled there, is increasingly competing with Marcellus/Utica gas (see “Free” NatGas in Texas Permian Changes Shale Gas Economics in M-U). The coming clash continues to grow. In a Bloomberg article published yesterday, we learn that the price of natgas in the Permian at major trading hubs is now lower than the price for hubs around the Marcellus/Utica, which is truly a first! We also get an ominous prediction from an analyst who watches these things, who said in the next three to four weeks, “natural gas prices in the Permian can go to zero because it’s literally a byproduct.” Free gas! As we pointed out in our previous post on Permian and gas prices, oil drillers can actually pay up to $2.36 per thousand cubic feet to dispose of the natgas coming out of Permian oil wells. That is, they can pay people to take the gas–as a cost of extracting the oil. Roughly one-third of the hydrocarbons coming from Permian wells is natgas. The biggest problem in the Permian for natgas is also the biggest problem in the M-U: lack of pipelines…

Read More “Natural Gas Prices in Texas Permian Drop Below Marcellus/Utica”

Last week MDN editor Jim Willis attended Hart Energy’s Marcellus-Utica Midstream conference in Pittsburgh (a series of stories are coming this week from that event). One of the stray comments Jim heard at the event was this: The chief rival or competitor to the Marcellus with respect to natural gas production is not, as you might assume (we sure did) the Haynesville Shale in Louisiana. No. The chief competitor, producing more and more volumes of natgas, is…the Permian! That’s right, an oil play! Why? When you drill for oil, you get other hydrocarbons out of the ground along with the oil. Primarily methane, or natural gas. It’s called “associated gas.” Even though most of what comes out of a Permian well is oil and not gas, because there are so darned many oil wells in the Permian (with more being drilled all the time), the total volume of gas coming from the Permian is going up, dramatically. The problem is, some Marcellus/Utica gas heads to the Gulf Coast to be used by petrochemical companies or to be exported. However, gas produced right there in the region is less expensive to get to market (shorter distance), so that Permian-sourced gas is competing, and increasingly crowding out, Marcellus/Utica gas. Investors have noticed and have, in a sense, “punished” some of the biggest of the big Marcellus/Utica producers by selling their shares, leading to a loss in share value. Among the hardest hit have been Southwestern Energy, Gulfport Energy, and Range Resources. The stock price for those three companies is down, since Jan. 1st, 33%, 30% and 25% respectively. A Bloomberg article says the stocks for those companies have been “mauled.” Indeed. Here’s some insight into how the Marcellus/Utica is increasingly going up against the oil giant Permian Basin, sometimes getting mauled…

Last week MDN editor Jim Willis attended Hart Energy’s Marcellus-Utica Midstream conference in Pittsburgh (a series of stories are coming this week from that event). One of the stray comments Jim heard at the event was this: The chief rival or competitor to the Marcellus with respect to natural gas production is not, as you might assume (we sure did) the Haynesville Shale in Louisiana. No. The chief competitor, producing more and more volumes of natgas, is…the Permian! That’s right, an oil play! Why? When you drill for oil, you get other hydrocarbons out of the ground along with the oil. Primarily methane, or natural gas. It’s called “associated gas.” Even though most of what comes out of a Permian well is oil and not gas, because there are so darned many oil wells in the Permian (with more being drilled all the time), the total volume of gas coming from the Permian is going up, dramatically. The problem is, some Marcellus/Utica gas heads to the Gulf Coast to be used by petrochemical companies or to be exported. However, gas produced right there in the region is less expensive to get to market (shorter distance), so that Permian-sourced gas is competing, and increasingly crowding out, Marcellus/Utica gas. Investors have noticed and have, in a sense, “punished” some of the biggest of the big Marcellus/Utica producers by selling their shares, leading to a loss in share value. Among the hardest hit have been Southwestern Energy, Gulfport Energy, and Range Resources. The stock price for those three companies is down, since Jan. 1st, 33%, 30% and 25% respectively. A Bloomberg article says the stocks for those companies have been “mauled.” Indeed. Here’s some insight into how the Marcellus/Utica is increasingly going up against the oil giant Permian Basin, sometimes getting mauled… This is a somewhat personal story that perfectly illustrates the point we’ve been making for years. MDN editor Jim Willis lives with his wife and family in the Binghamton, NY area. Jim likes to say he “lives behind enemy lines”–meaning New York State under Andrew Cuomo and his radical left base are hostile to the fossil fuel industry. The cost of Cuomo’s actions for every New Yorker (at least those of us living in Upstate) is now on full display for all to see. A few weeks ago Jim got his monthly electric bill from New York State Electric & Gas (NYSEG, owned by the Spanish company Iberdrola). Jim’s eyes about fell out of their sockets. Jim largely uses electricity for heating (with a fuel oil furnace as backup). No natural gas lines where Jim lives, unfortunately. Even in the dead of winter Jim’s electric bill is rarely over $200 in any given month–typically around $150. This time? Nearly $700!!!! At first, Jim chalked it up to the cold snap and the constant running of his electric heat source. Then he spotted an article (below, sent to us by Vic Furman), that shows Jim is not the only one. Across the entire region folks received bills that are double and triple the usual amount. Why the spike in price? It seems the lack of natural gas via pipelines is not only hurting New England, it’s now hurting Upstate NY. Due to a lack of natgas supplies and the huge regional demand for natgas–for home heating as well as for electric generators–the spot price for gas went through the roof and along with it NYSEG’s cost for both natgas and electricity generated by natgas also went through the roof. Consequently, Cuomo’s frack ban and (now) pipeline ban on importing natgas from PA are having very real, tangible consequences–in our electric bills. All of Cuomo’s precious renewable sources of energy will not, indeed cannot, make up for a lack of natgas. Cuomo’s stupidity is costing ME real money…

This is a somewhat personal story that perfectly illustrates the point we’ve been making for years. MDN editor Jim Willis lives with his wife and family in the Binghamton, NY area. Jim likes to say he “lives behind enemy lines”–meaning New York State under Andrew Cuomo and his radical left base are hostile to the fossil fuel industry. The cost of Cuomo’s actions for every New Yorker (at least those of us living in Upstate) is now on full display for all to see. A few weeks ago Jim got his monthly electric bill from New York State Electric & Gas (NYSEG, owned by the Spanish company Iberdrola). Jim’s eyes about fell out of their sockets. Jim largely uses electricity for heating (with a fuel oil furnace as backup). No natural gas lines where Jim lives, unfortunately. Even in the dead of winter Jim’s electric bill is rarely over $200 in any given month–typically around $150. This time? Nearly $700!!!! At first, Jim chalked it up to the cold snap and the constant running of his electric heat source. Then he spotted an article (below, sent to us by Vic Furman), that shows Jim is not the only one. Across the entire region folks received bills that are double and triple the usual amount. Why the spike in price? It seems the lack of natural gas via pipelines is not only hurting New England, it’s now hurting Upstate NY. Due to a lack of natgas supplies and the huge regional demand for natgas–for home heating as well as for electric generators–the spot price for gas went through the roof and along with it NYSEG’s cost for both natgas and electricity generated by natgas also went through the roof. Consequently, Cuomo’s frack ban and (now) pipeline ban on importing natgas from PA are having very real, tangible consequences–in our electric bills. All of Cuomo’s precious renewable sources of energy will not, indeed cannot, make up for a lack of natgas. Cuomo’s stupidity is costing ME real money… The price of natural gas is a complicated subject. First, “the price” is never just “the price.” Many people look to the NYMEX or Henry Hub spot price as “the price.” Indeed, most of the financial contracts for natural gas are based on the Henry Hub price. However, as we’ve written many times over the years, gas is bought and sold at hundreds of points along major interstate natural gas pipelines. The price at one place on a pipeline, like the Tennessee Gas Pipeline Zone 4 in northeastern Pennsylvania, is vastly different from the Henry Hub. Price is dependent on many factors–supply and demand to be sure. But also weather. Weather is probably the biggest influencer of natgas prices. Why? The warmer (or colder) it is, the more natural gas is used to cool or heat homes and businesses. The more demand, the higher the price. Conversely, the less demand, the lower the price. Henry Hub is a useful yardstick and the most-watched natural gas price in the world. Our favorite government agency, the U.S. Energy Information Administration, recently published their Short-Term Energy Outlook (STEO). In the STEO, EIA predicts the price of natural gas at Henry Hub will remain relatively flat both this year and next year. This year (2018), EIA says the average price of gas at Henry Hub will be $2.88 per thousand cubic feet (Mcf). Next year? EIA says the price will average $2.92/Mcf. The average price of gas at Henry Hub for all of 2017 was $2.99/Mcf. Bottom line: The price of gas is a bit depressing for gas drillers for the foreseeable future. Here’s EIA’s reasoning…

The price of natural gas is a complicated subject. First, “the price” is never just “the price.” Many people look to the NYMEX or Henry Hub spot price as “the price.” Indeed, most of the financial contracts for natural gas are based on the Henry Hub price. However, as we’ve written many times over the years, gas is bought and sold at hundreds of points along major interstate natural gas pipelines. The price at one place on a pipeline, like the Tennessee Gas Pipeline Zone 4 in northeastern Pennsylvania, is vastly different from the Henry Hub. Price is dependent on many factors–supply and demand to be sure. But also weather. Weather is probably the biggest influencer of natgas prices. Why? The warmer (or colder) it is, the more natural gas is used to cool or heat homes and businesses. The more demand, the higher the price. Conversely, the less demand, the lower the price. Henry Hub is a useful yardstick and the most-watched natural gas price in the world. Our favorite government agency, the U.S. Energy Information Administration, recently published their Short-Term Energy Outlook (STEO). In the STEO, EIA predicts the price of natural gas at Henry Hub will remain relatively flat both this year and next year. This year (2018), EIA says the average price of gas at Henry Hub will be $2.88 per thousand cubic feet (Mcf). Next year? EIA says the price will average $2.92/Mcf. The average price of gas at Henry Hub for all of 2017 was $2.99/Mcf. Bottom line: The price of gas is a bit depressing for gas drillers for the foreseeable future. Here’s EIA’s reasoning… Anyone with even a passing interest in the natural gas market–either the Marcellus/Utica or elsewhere–knows there is one dominant factor that drives exploration and production: PRICE. The price of natural gas is the tail that wags the entire natgas dog. Low price? Less (or no) drilling, shut-in wells, less leasing–everything is less. High price? Pop the cork on the champagne bottle! When the price goes up and stays up, drillers begin seismic surveys, then leasing, then permits, then drilling. After drilling comes pipelines–both to the well and to market. And businesses tend to gather around points where there is access to natgas (and its byproducts). It’s a virtuous cycle, from upstream (drilling) to midstream (pipelines) to downstream (end users of the gas)–that all starts with price. Who should have an interest in price? Everybody! However, there are some whose jobs and livelihoods depend on price–gas traders, industrial buyers, drillers who need to sell their gas, etc. Those people need a daily update on the price. Who do they turn to? There are several price reporting authorities that monitor trade information for natural gas trading. There is no single price for natural gas–there are hundreds of prices. Gas is traded at trading hubs or points along major pipelines across the country. Each time a trade is done (price requested, price offered or “ask” and “bid”), that valuable information gets recorded and sent to a price recording authority. Each day around 1:30 PM Central Time, NGI gathers up trade information for THAT DAY, trades that have occurred so far at trading points all over the US and Canada, and posts/emails the information to subscribers. It is like getting tomorrow’s prices–the prices everyone else will base their trades on–today! How can you get tomorrow’s prices today? Glad you asked.

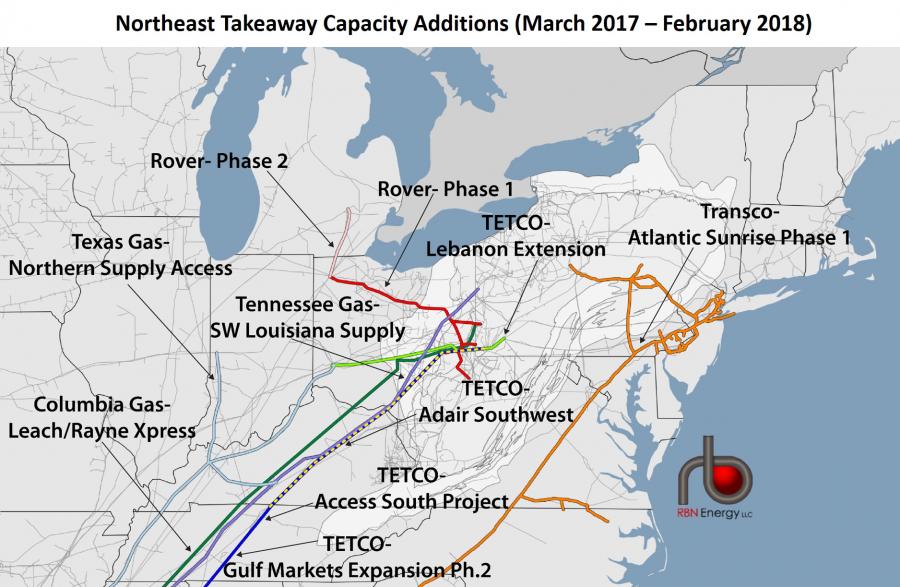

Anyone with even a passing interest in the natural gas market–either the Marcellus/Utica or elsewhere–knows there is one dominant factor that drives exploration and production: PRICE. The price of natural gas is the tail that wags the entire natgas dog. Low price? Less (or no) drilling, shut-in wells, less leasing–everything is less. High price? Pop the cork on the champagne bottle! When the price goes up and stays up, drillers begin seismic surveys, then leasing, then permits, then drilling. After drilling comes pipelines–both to the well and to market. And businesses tend to gather around points where there is access to natgas (and its byproducts). It’s a virtuous cycle, from upstream (drilling) to midstream (pipelines) to downstream (end users of the gas)–that all starts with price. Who should have an interest in price? Everybody! However, there are some whose jobs and livelihoods depend on price–gas traders, industrial buyers, drillers who need to sell their gas, etc. Those people need a daily update on the price. Who do they turn to? There are several price reporting authorities that monitor trade information for natural gas trading. There is no single price for natural gas–there are hundreds of prices. Gas is traded at trading hubs or points along major pipelines across the country. Each time a trade is done (price requested, price offered or “ask” and “bid”), that valuable information gets recorded and sent to a price recording authority. Each day around 1:30 PM Central Time, NGI gathers up trade information for THAT DAY, trades that have occurred so far at trading points all over the US and Canada, and posts/emails the information to subscribers. It is like getting tomorrow’s prices–the prices everyone else will base their trades on–today! How can you get tomorrow’s prices today? Glad you asked.  In the fourth quarter of 2017 (Oct-Dec), 2.3 billion cubic feet per day (Bcf/d) of new/extra pipeline capacity was added in the Marcellus/Utica region, to carry our gas to markets outside the region. Even though production in the Marcellus/Utica has continued to climb every single month, that 2.3 Bcf/d of extra “takeaway” capacity had an immediate effect–prices for our gas began to rise. Here’s a bit of exciting news: By the end of the first quarter this year (that is, by Mar. 31st), another 3 Bcf/d of pipeline takeaway capacity will be online. We expect this new takeaway, combined with last quarter’s increase in takeaway, will continue to drive prices for our gas higher…

In the fourth quarter of 2017 (Oct-Dec), 2.3 billion cubic feet per day (Bcf/d) of new/extra pipeline capacity was added in the Marcellus/Utica region, to carry our gas to markets outside the region. Even though production in the Marcellus/Utica has continued to climb every single month, that 2.3 Bcf/d of extra “takeaway” capacity had an immediate effect–prices for our gas began to rise. Here’s a bit of exciting news: By the end of the first quarter this year (that is, by Mar. 31st), another 3 Bcf/d of pipeline takeaway capacity will be online. We expect this new takeaway, combined with last quarter’s increase in takeaway, will continue to drive prices for our gas higher… In the end, even the ultra-liberal editors of the Boston Globe couldn’t ignore and deny reality–the reality that their own favorite sons and daughters are to blame for sky high energy prices and dirtier air, because they’ve fought against new natural gas pipelines. We’ve been blowing the horn that New England is getting hosed on energy prices, paying the highest average prices in the world for natural gas, because of their stubborn refusal to allow new Marcellus gas pipelines into the region (see

In the end, even the ultra-liberal editors of the Boston Globe couldn’t ignore and deny reality–the reality that their own favorite sons and daughters are to blame for sky high energy prices and dirtier air, because they’ve fought against new natural gas pipelines. We’ve been blowing the horn that New England is getting hosed on energy prices, paying the highest average prices in the world for natural gas, because of their stubborn refusal to allow new Marcellus gas pipelines into the region (see  Baby it’s cold outside! This was predictable (and indeed, MDN did predict it). With the arrival of an extended cold period, because of a lack of natural gas pipeline capacity in New England, recent spot prices for natgas near Boston have spiked to more than $35 per thousand cubic feet (Mcf). It gives New England the dubious distinction of paying the highest average price for natural gas in the entire WORLD. The price for the same gas about 250 miles away in the Marcellus? Between $1-$2/Mcf. And yet the dunderheads in New England, like U.S. Sen. Elizabeth “Pocahontas” Warren, continue to block new pipelines in the region. “Stupid is as stupid does,” as Forrest Gump said. We hope our friends in New England enjoy paying through the nose and every other orifice they possess over the next few weeks, until the arctic blast subsides…

Baby it’s cold outside! This was predictable (and indeed, MDN did predict it). With the arrival of an extended cold period, because of a lack of natural gas pipeline capacity in New England, recent spot prices for natgas near Boston have spiked to more than $35 per thousand cubic feet (Mcf). It gives New England the dubious distinction of paying the highest average price for natural gas in the entire WORLD. The price for the same gas about 250 miles away in the Marcellus? Between $1-$2/Mcf. And yet the dunderheads in New England, like U.S. Sen. Elizabeth “Pocahontas” Warren, continue to block new pipelines in the region. “Stupid is as stupid does,” as Forrest Gump said. We hope our friends in New England enjoy paying through the nose and every other orifice they possess over the next few weeks, until the arctic blast subsides… American shale has fundamentally transformed the world geopolitically. How? Just think about. #1 – Saudi Arabia and Iran are on the brink of all-out war. For decades Saudia Arabia has been the world’s leading oil producing country. Iran has been in the top five oil producing counties. #2 – Venezuela, the country with the world’s largest oil reserves, is rumored to have defaulted on its foreign debt. Either situation, #1 or #2, hint at the potential for the flow of oil to be disrupted. Both happening at the same time is an oil cataclysm. A decade ago such news would have resulted in oil hitting $100, perhaps even $150 per barrel. The price of gas at the pump would have soared, overnight, to more than $5/gallon. Yet what has happened to the price of oil with this recent geopolitical news? Nothing. If anything, the price has gone down! The only reason oil prices are not through the roof is because of the abundance of American shale oil. An occasional guest blogger here on MDN is Daniel Markind, a partner with law firm

American shale has fundamentally transformed the world geopolitically. How? Just think about. #1 – Saudi Arabia and Iran are on the brink of all-out war. For decades Saudia Arabia has been the world’s leading oil producing country. Iran has been in the top five oil producing counties. #2 – Venezuela, the country with the world’s largest oil reserves, is rumored to have defaulted on its foreign debt. Either situation, #1 or #2, hint at the potential for the flow of oil to be disrupted. Both happening at the same time is an oil cataclysm. A decade ago such news would have resulted in oil hitting $100, perhaps even $150 per barrel. The price of gas at the pump would have soared, overnight, to more than $5/gallon. Yet what has happened to the price of oil with this recent geopolitical news? Nothing. If anything, the price has gone down! The only reason oil prices are not through the roof is because of the abundance of American shale oil. An occasional guest blogger here on MDN is Daniel Markind, a partner with law firm

Last week the Federal Energy Regulatory Commission’s (FERC) Office of Enforcement (OE) released their 2017-18 Winter Energy Market Assessment, an annual look ahead to the coming winter. OE shares their thoughts and expectations about market preparedness, including an assessment of risks. What does the report show? OE says production is going up (increasing another 5 billion cubic feet per day by next April), natural gas in storage is “robust” (meaning high), and the upcoming winter weather looks to be warmer than normal in most of the country, including the northeast. Translation: Don’t expect the price of natural gas to spike this winter. Prices will remain relatively low. Here’s the full OE report (interesting reading, pretty charts)…

Last week the Federal Energy Regulatory Commission’s (FERC) Office of Enforcement (OE) released their 2017-18 Winter Energy Market Assessment, an annual look ahead to the coming winter. OE shares their thoughts and expectations about market preparedness, including an assessment of risks. What does the report show? OE says production is going up (increasing another 5 billion cubic feet per day by next April), natural gas in storage is “robust” (meaning high), and the upcoming winter weather looks to be warmer than normal in most of the country, including the northeast. Translation: Don’t expect the price of natural gas to spike this winter. Prices will remain relatively low. Here’s the full OE report (interesting reading, pretty charts)… With new pipelines coming online in the Marcellus/Utica, will the price of natural gas bought and sold at regional trading points, like Dominion South and TGP (Tennessee Gas Pipeline) Zone 4 go higher? It certainly makes sense that with more of our gas flowing out of the area, there will be less gas left in the area and therefore will fetch a higher price. In fact, just after Energy Transfer’s Rover Pipeline, now in partial service, began to flow, the price of gas at the Dominion South hub jumped 31% (see

With new pipelines coming online in the Marcellus/Utica, will the price of natural gas bought and sold at regional trading points, like Dominion South and TGP (Tennessee Gas Pipeline) Zone 4 go higher? It certainly makes sense that with more of our gas flowing out of the area, there will be less gas left in the area and therefore will fetch a higher price. In fact, just after Energy Transfer’s Rover Pipeline, now in partial service, began to flow, the price of gas at the Dominion South hub jumped 31% (see  Once upon a time the Environmental Defense Fund (EDF) held out the veneer of practical environmentalism–people who would at least listen to the fossil fuel industry and in some rare cases, reach their hand across the isle to work on initiatives with the industry (for example, they are a partner in the Pittsburgh-based Center for Responsible Shale Development). But over the past few years that veneer has been stripped off, and now the EDF has been exposed as a hack organization, just like all the rest of the loons on the left. Case in point is their latest propaganda, issued last week. The EDF published a “report” that makes the rather preposterous claim that New England customers have overpaid utility bills by $3.6 billion due to collusion between the natural gas and electricity industries. EDF spins the outlandish theory that Avangrid and Eversource brilliantly conspired to create Enron-style fake gas shortages involving a whopping 3.5% of the capacity of the Algonquin pipeline–all in order to drive up electric clearing prices for a wind farm Avangrid didn’t yet own, a rarely dispatched Avangrid oil peaker run under rate of return, and three crappy, rarely operated oil and coal plants in New Hampshire–plus nine little hydro dams that Eversource was trying to unload for years (finally sold last week). EDF’s tall tale is so bizarre (and hard to follow) it’s laughable. However, mainstream fake news media picks it up and regurgitates it to an unsuspecting public, so we’re here to set the record straight on yet another Big Green hoax…

Once upon a time the Environmental Defense Fund (EDF) held out the veneer of practical environmentalism–people who would at least listen to the fossil fuel industry and in some rare cases, reach their hand across the isle to work on initiatives with the industry (for example, they are a partner in the Pittsburgh-based Center for Responsible Shale Development). But over the past few years that veneer has been stripped off, and now the EDF has been exposed as a hack organization, just like all the rest of the loons on the left. Case in point is their latest propaganda, issued last week. The EDF published a “report” that makes the rather preposterous claim that New England customers have overpaid utility bills by $3.6 billion due to collusion between the natural gas and electricity industries. EDF spins the outlandish theory that Avangrid and Eversource brilliantly conspired to create Enron-style fake gas shortages involving a whopping 3.5% of the capacity of the Algonquin pipeline–all in order to drive up electric clearing prices for a wind farm Avangrid didn’t yet own, a rarely dispatched Avangrid oil peaker run under rate of return, and three crappy, rarely operated oil and coal plants in New Hampshire–plus nine little hydro dams that Eversource was trying to unload for years (finally sold last week). EDF’s tall tale is so bizarre (and hard to follow) it’s laughable. However, mainstream fake news media picks it up and regurgitates it to an unsuspecting public, so we’re here to set the record straight on yet another Big Green hoax… Each year the consultants at Deloitte conduct a survey of oil and gas industry professionals. Last year the survey showed o&g execs believed we were already in the midst of a recovery for the industry (see

Each year the consultants at Deloitte conduct a survey of oil and gas industry professionals. Last year the survey showed o&g execs believed we were already in the midst of a recovery for the industry (see