7 Major Marcellus/Utica Pipelines Coming This Year & Next

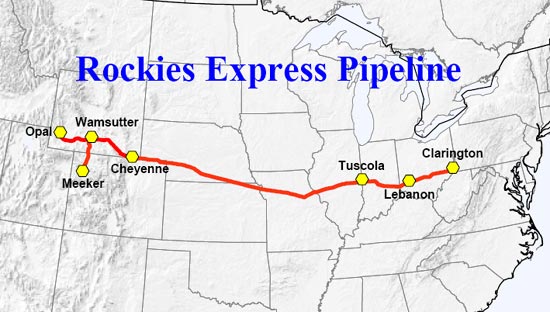

Yesterday MDN brought you a story about the difference, in the price drillers get for their gas, that a single pipeline can make (see The Difference One Utica Pipeline Can Make on Gas Prices). That story was about how the Rockies Express Pipeline (REX) reversed its flow from Ohio to Missouri adding 800 million cubic feet per day (MMcf/d) of extra capacity for a total of 2.6 billion cubic feet per day (Bcf/d) of gas now flowing from the Utica/Marcellus to the Midwest. REX is an existing pipeline. Just think about all of the pipeline projects in the queue for the Marcellus/Utica. In fact, there are seven major projects that are either already-approved by the Federal Energy Regulatory Commission (FERC) or under review now. If you add them all together, it represents almost 12 Bcf/d of additional natural gas flowing out of our region to other regions, where it will fetch higher prices. What are the seven projects? How much gas will each flow? When will they go online? We need a scorecard! We now have one…

Yesterday MDN brought you a story about the difference, in the price drillers get for their gas, that a single pipeline can make (see The Difference One Utica Pipeline Can Make on Gas Prices). That story was about how the Rockies Express Pipeline (REX) reversed its flow from Ohio to Missouri adding 800 million cubic feet per day (MMcf/d) of extra capacity for a total of 2.6 billion cubic feet per day (Bcf/d) of gas now flowing from the Utica/Marcellus to the Midwest. REX is an existing pipeline. Just think about all of the pipeline projects in the queue for the Marcellus/Utica. In fact, there are seven major projects that are either already-approved by the Federal Energy Regulatory Commission (FERC) or under review now. If you add them all together, it represents almost 12 Bcf/d of additional natural gas flowing out of our region to other regions, where it will fetch higher prices. What are the seven projects? How much gas will each flow? When will they go online? We need a scorecard! We now have one…

Read More “7 Major Marcellus/Utica Pipelines Coming This Year & Next”

Major multinational bank Société Générale, headquartered in Paris but with major operations here in the U.S., has just issued a 37-page report on U.S. commodities. The theme of the report caught our attention: “Five facts about shale: it’s coming back, and coming back strong.” Analysts working for Société Générale asked themselves this question: Will the U.S. recovery in oil and gas production offset OPEC cuts? They review some of the key dynamics of U.S. shale production in their report. Specifically, they highlight five facts about U.S. shale production that all point to the same underlying trend: shale is coming back in a big way…

Major multinational bank Société Générale, headquartered in Paris but with major operations here in the U.S., has just issued a 37-page report on U.S. commodities. The theme of the report caught our attention: “Five facts about shale: it’s coming back, and coming back strong.” Analysts working for Société Générale asked themselves this question: Will the U.S. recovery in oil and gas production offset OPEC cuts? They review some of the key dynamics of U.S. shale production in their report. Specifically, they highlight five facts about U.S. shale production that all point to the same underlying trend: shale is coming back in a big way…

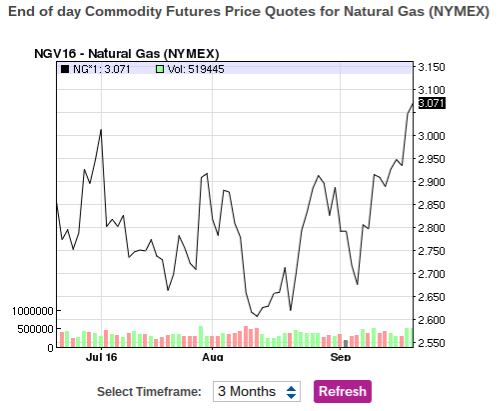

Good news for natural gas drillers in general, and Marcellus/Utica drillers in particular: Our favorite government agency, the U.S. Energy Information Administration (EIA) predicts the average price for natural gas in the U.S. will rise in both 2017 and 2018. EIA expects the Henry Hub natural gas spot price to average $3.55 per million British thermal units (MMBtu) in 2017 and $3.73/MMBtu in 2018, both higher than the 2016 average of $2.51/MMBtu. Higher prices in 2017 and 2018 reflect natural gas consumption and exports exceeding supply and imports, leading to lower average inventory levels…

Good news for natural gas drillers in general, and Marcellus/Utica drillers in particular: Our favorite government agency, the U.S. Energy Information Administration (EIA) predicts the average price for natural gas in the U.S. will rise in both 2017 and 2018. EIA expects the Henry Hub natural gas spot price to average $3.55 per million British thermal units (MMBtu) in 2017 and $3.73/MMBtu in 2018, both higher than the 2016 average of $2.51/MMBtu. Higher prices in 2017 and 2018 reflect natural gas consumption and exports exceeding supply and imports, leading to lower average inventory levels… How low can you go? Natural gas spot prices in 2016 averaged $2.49 per thousand cubic feet (Mcf), or more commonly per million British thermal units (MMBtu) at the national benchmark Henry Hub. That is the lowest annual average price for natgas since 1999. The monthly average price fell below $2.00/Mcf from February through May, but later increased, ending the year at an average of $3.58/Mcf in December. Marcellus/Utica drillers would LOVE to see prices like $2.49 or $3.58. Prices in the northeast, because of lack of takeaway pipelines, sometimes sank below $1/Mcf at certain trading points…

How low can you go? Natural gas spot prices in 2016 averaged $2.49 per thousand cubic feet (Mcf), or more commonly per million British thermal units (MMBtu) at the national benchmark Henry Hub. That is the lowest annual average price for natgas since 1999. The monthly average price fell below $2.00/Mcf from February through May, but later increased, ending the year at an average of $3.58/Mcf in December. Marcellus/Utica drillers would LOVE to see prices like $2.49 or $3.58. Prices in the northeast, because of lack of takeaway pipelines, sometimes sank below $1/Mcf at certain trading points… In September, MDN brought you research on 10 of the largest Marcellus/Utica drillers that have “hedged” their 2017 production (see

In September, MDN brought you research on 10 of the largest Marcellus/Utica drillers that have “hedged” their 2017 production (see  Every now and again it’s fun to read Peak Oil people and their wild theories that oil will run out any year now. Such theories have been exposed as complete bunkum, mainly because those crusty old guys (and gals) in the U.S. oil patch keep figuring out how to do new things to extract oil, at cheaper prices. Technology gets better, procedures get better, we do more with less. And we produce more oil, year after year. But it’s still good to read those with a different viewpoint from time to time, just to keep us on our toes. Sometimes they even make some good points. That’s what we found in an article that posits the theory that shale oil really isn’t as good as it may appear. Why? According to this peak oil author, better technology now being used is not nearly as important as the technique currently employed called “high grading”–or targeting the sweetest of the sweet spots, which are far more productive than the run-of-the-mill drilling locations. The author maintains we’ll run out the best areas to drill soon, leaving us with less-than-optimal areas and therefore much higher costs. And then shale is toast. That’s the theory anyway…

Every now and again it’s fun to read Peak Oil people and their wild theories that oil will run out any year now. Such theories have been exposed as complete bunkum, mainly because those crusty old guys (and gals) in the U.S. oil patch keep figuring out how to do new things to extract oil, at cheaper prices. Technology gets better, procedures get better, we do more with less. And we produce more oil, year after year. But it’s still good to read those with a different viewpoint from time to time, just to keep us on our toes. Sometimes they even make some good points. That’s what we found in an article that posits the theory that shale oil really isn’t as good as it may appear. Why? According to this peak oil author, better technology now being used is not nearly as important as the technique currently employed called “high grading”–or targeting the sweetest of the sweet spots, which are far more productive than the run-of-the-mill drilling locations. The author maintains we’ll run out the best areas to drill soon, leaving us with less-than-optimal areas and therefore much higher costs. And then shale is toast. That’s the theory anyway… Once a month our favorite government agency, the U.S. Energy Information Administration (EIA), issues a Short-Term Energy Outlook (STEO). The EIA issued their latest edition on Tuesday. We have a full copy below. We’ve grabbed out the section on natural gas because it includes a couple of key points: (1) EIA predicts that natural gas production in the U.S. for 2016 will see a healthy decline over 2015 levels–1.3 billion cubic feet per day (Bcf/d) less in 2016. That’s the first annual production decline since 2005! (2) The EIA predicts the average price for natural gas at the benchmark Henry Hub will climb from $2.49/Mcf (thousand cubic feet) in 2016 to a whopping $3.27/Mcf in 2017. Why the jump? Growing domestic natural gas consumption, along with higher pipeline exports to Mexico and liquefied natural gas exports. Here’s the natgas section of the STEO, along with a copy of the full report…

Once a month our favorite government agency, the U.S. Energy Information Administration (EIA), issues a Short-Term Energy Outlook (STEO). The EIA issued their latest edition on Tuesday. We have a full copy below. We’ve grabbed out the section on natural gas because it includes a couple of key points: (1) EIA predicts that natural gas production in the U.S. for 2016 will see a healthy decline over 2015 levels–1.3 billion cubic feet per day (Bcf/d) less in 2016. That’s the first annual production decline since 2005! (2) The EIA predicts the average price for natural gas at the benchmark Henry Hub will climb from $2.49/Mcf (thousand cubic feet) in 2016 to a whopping $3.27/Mcf in 2017. Why the jump? Growing domestic natural gas consumption, along with higher pipeline exports to Mexico and liquefied natural gas exports. Here’s the natgas section of the STEO, along with a copy of the full report… Middle Eastern counties who sell us oil, including Saudi Arabia, have never been our “friends.” To pretend otherwise is dangerously stupid. We have depended on them for their oil, plain and simple. Oil equals energy and energy equals freedom and prosperity for the U.S. In the 1970s OPEC, the Organization of the Petroleum Exporting Countries, flexed its economic muscles against our country and brought us to our knees with an oil embargo that caused shortages and prices to skyrocket. MDN editor Jim Willis recalls growing up in the 1970s when gas was rationed and you could only buy gas every few days (odd and even days) based on your license plate number. A scary time in our country. Thing is, our enemies haven’t changed–they are still there. They’re just a whole lot richer than they were back then, richer with our money in their pockets. The shale revolution changed all that. We are close to being 100% energy independent–without the need to import oil. Oh, we’ll have to keep importing for the foreseeable future. We don’t have enough refineries here to process the type of oil we produce (light sweet crude). But in a pinch, we’d figure out a way. OPEC and Saudi Arabia have badly misjudged America. They thought they could flood the market with cheap oil and bankrupt America’s shale drillers. Didn’t happen. In fact, we got better. We figured out how to drill for less money. Little known fact: Bakken drillers can now make money with oil selling as low as $29 per barrel! In other words, it’s now time to put the last nail in OPEC’s coffin and kiss them goodbye. We sincerely hope finally defeating OPEC will be a top priority in the new Trump Administration…

Middle Eastern counties who sell us oil, including Saudi Arabia, have never been our “friends.” To pretend otherwise is dangerously stupid. We have depended on them for their oil, plain and simple. Oil equals energy and energy equals freedom and prosperity for the U.S. In the 1970s OPEC, the Organization of the Petroleum Exporting Countries, flexed its economic muscles against our country and brought us to our knees with an oil embargo that caused shortages and prices to skyrocket. MDN editor Jim Willis recalls growing up in the 1970s when gas was rationed and you could only buy gas every few days (odd and even days) based on your license plate number. A scary time in our country. Thing is, our enemies haven’t changed–they are still there. They’re just a whole lot richer than they were back then, richer with our money in their pockets. The shale revolution changed all that. We are close to being 100% energy independent–without the need to import oil. Oh, we’ll have to keep importing for the foreseeable future. We don’t have enough refineries here to process the type of oil we produce (light sweet crude). But in a pinch, we’d figure out a way. OPEC and Saudi Arabia have badly misjudged America. They thought they could flood the market with cheap oil and bankrupt America’s shale drillers. Didn’t happen. In fact, we got better. We figured out how to drill for less money. Little known fact: Bakken drillers can now make money with oil selling as low as $29 per barrel! In other words, it’s now time to put the last nail in OPEC’s coffin and kiss them goodbye. We sincerely hope finally defeating OPEC will be a top priority in the new Trump Administration…

One company that has been really smart and savvy when it comes to hedging is Antero Resources. Earlier this year when the average price of natural gas was selling for under $3 per thousand cubic feet (Mcf) on the benchmark Henry Hub, Antero averaged a sale price of $4.54/Mcf–in the Marcellus/Utica! Where prices are always BELOW the Henry Hub (see

One company that has been really smart and savvy when it comes to hedging is Antero Resources. Earlier this year when the average price of natural gas was selling for under $3 per thousand cubic feet (Mcf) on the benchmark Henry Hub, Antero averaged a sale price of $4.54/Mcf–in the Marcellus/Utica! Where prices are always BELOW the Henry Hub (see  We hate to say “I told you so,” but we’ll say it anyway. If you live in New England, prepare yourself. You’re about to experience more price shocks for natural gas and electricity (4x more than the rest of the country, or higher). Why? Because you’re blocking new pipeline projects that would bring cheap, abundant, clean-burning natural gas to the region. The Pennsylvania Marcellus Shale sits a few hundred miles away–yet very little Marcellus gas is flowing to New England at this point. New England, more than any other region in the country, relies on natgas to power electric generating plants. Without extra supplies, especially in the winter months when natgas gets used for heating, electric generators are forced to pay obscenely high rates to stay in operation. Those obscenely high rates get passed along to ratepayers–businesses AND residences. Yet anti-fossil fuel wackos continue to try and stop new pipelines, sometimes criminally (see

We hate to say “I told you so,” but we’ll say it anyway. If you live in New England, prepare yourself. You’re about to experience more price shocks for natural gas and electricity (4x more than the rest of the country, or higher). Why? Because you’re blocking new pipeline projects that would bring cheap, abundant, clean-burning natural gas to the region. The Pennsylvania Marcellus Shale sits a few hundred miles away–yet very little Marcellus gas is flowing to New England at this point. New England, more than any other region in the country, relies on natgas to power electric generating plants. Without extra supplies, especially in the winter months when natgas gets used for heating, electric generators are forced to pay obscenely high rates to stay in operation. Those obscenely high rates get passed along to ratepayers–businesses AND residences. Yet anti-fossil fuel wackos continue to try and stop new pipelines, sometimes criminally (see  On Sept. 30 MDN editor Jim Willis attended S&P Global Platts’

On Sept. 30 MDN editor Jim Willis attended S&P Global Platts’  Last winter was pretty unusual by everyone’s standards. It was much warmer and less snowy than normal in the northeast, and natural gas production/levels remained high over the course of the winter. It meant that the price of natural gas stayed in the basement during the time of year when it normally at least makes it to the first floor. What about this year? MDN recently reported that it’s going to be colder and snowier than average in the northeast this year (see

Last winter was pretty unusual by everyone’s standards. It was much warmer and less snowy than normal in the northeast, and natural gas production/levels remained high over the course of the winter. It meant that the price of natural gas stayed in the basement during the time of year when it normally at least makes it to the first floor. What about this year? MDN recently reported that it’s going to be colder and snowier than average in the northeast this year (see