One of our favorite Marcellus drillers, Cabot Oil & Gas, issued their second quarter 2018 update on Friday. Some of the highlights include: net income doubling, from $21.5 million to $42.4 million year over year; drilled 24 and completed 23 wells (down just a tad y/y, from 27 drilled and 26 completed in 2Q17); and Marcellus production was 1.89 billion cubic feet per day (Bcf/d), a new all-time high, up 4% from first quarter 2018. Cabot’s CEO Dan Dinges talked about the company ending its dalliance with the Permian Basin, shutting down “exploratory area #1” in 2Q18, but continuing work on “exploratory area #2”–which is in central Ohio. He said more details on Ohio exploration will be forthcoming in the Q3 update. As we looked through the official update, the PowerPoint slide deck and a transcript of the conference call (all below), we found a few more items that caught our interest. (1) Cabot says they have another 35 years worth of drilling to do in the Marcellus, with the current leases they have in place. (2) The “break even” price at which they begin to make money has now gone all the way down to just under one dollar per Mcf. (3) The company’s plans still count on the Constitution Pipeline getting built. (4) Train 1 of the Lackawanna Energy Center (gas-fired electric plant near Scranton) is up and running and burning 70 Mmcf/d of Cabot’s Marcellus gas, train 2 will be online by October 1st, and train 3 by December 1st. Here’s the good news from Cabot…

One of our favorite Marcellus drillers, Cabot Oil & Gas, issued their second quarter 2018 update on Friday. Some of the highlights include: net income doubling, from $21.5 million to $42.4 million year over year; drilled 24 and completed 23 wells (down just a tad y/y, from 27 drilled and 26 completed in 2Q17); and Marcellus production was 1.89 billion cubic feet per day (Bcf/d), a new all-time high, up 4% from first quarter 2018. Cabot’s CEO Dan Dinges talked about the company ending its dalliance with the Permian Basin, shutting down “exploratory area #1” in 2Q18, but continuing work on “exploratory area #2”–which is in central Ohio. He said more details on Ohio exploration will be forthcoming in the Q3 update. As we looked through the official update, the PowerPoint slide deck and a transcript of the conference call (all below), we found a few more items that caught our interest. (1) Cabot says they have another 35 years worth of drilling to do in the Marcellus, with the current leases they have in place. (2) The “break even” price at which they begin to make money has now gone all the way down to just under one dollar per Mcf. (3) The company’s plans still count on the Constitution Pipeline getting built. (4) Train 1 of the Lackawanna Energy Center (gas-fired electric plant near Scranton) is up and running and burning 70 Mmcf/d of Cabot’s Marcellus gas, train 2 will be online by October 1st, and train 3 by December 1st. Here’s the good news from Cabot…

Read More “Cabot O&G 2Q18: Income Doubles, Drilled 24 Wells, Ends Permian”

Last Friday Cabot Oil & Gas released its full year 2018 (and 4Q18) update, proclaiming 2018 was the best year ever for Cabot financially in the past almost 30 years the company has publicly traded shares of stock. The company hit new record natural gas production of 735 billion cubic feet equivalent (Bcfe) in 2018 (roughly 2 Bcfe/d), up 7% from 2017.

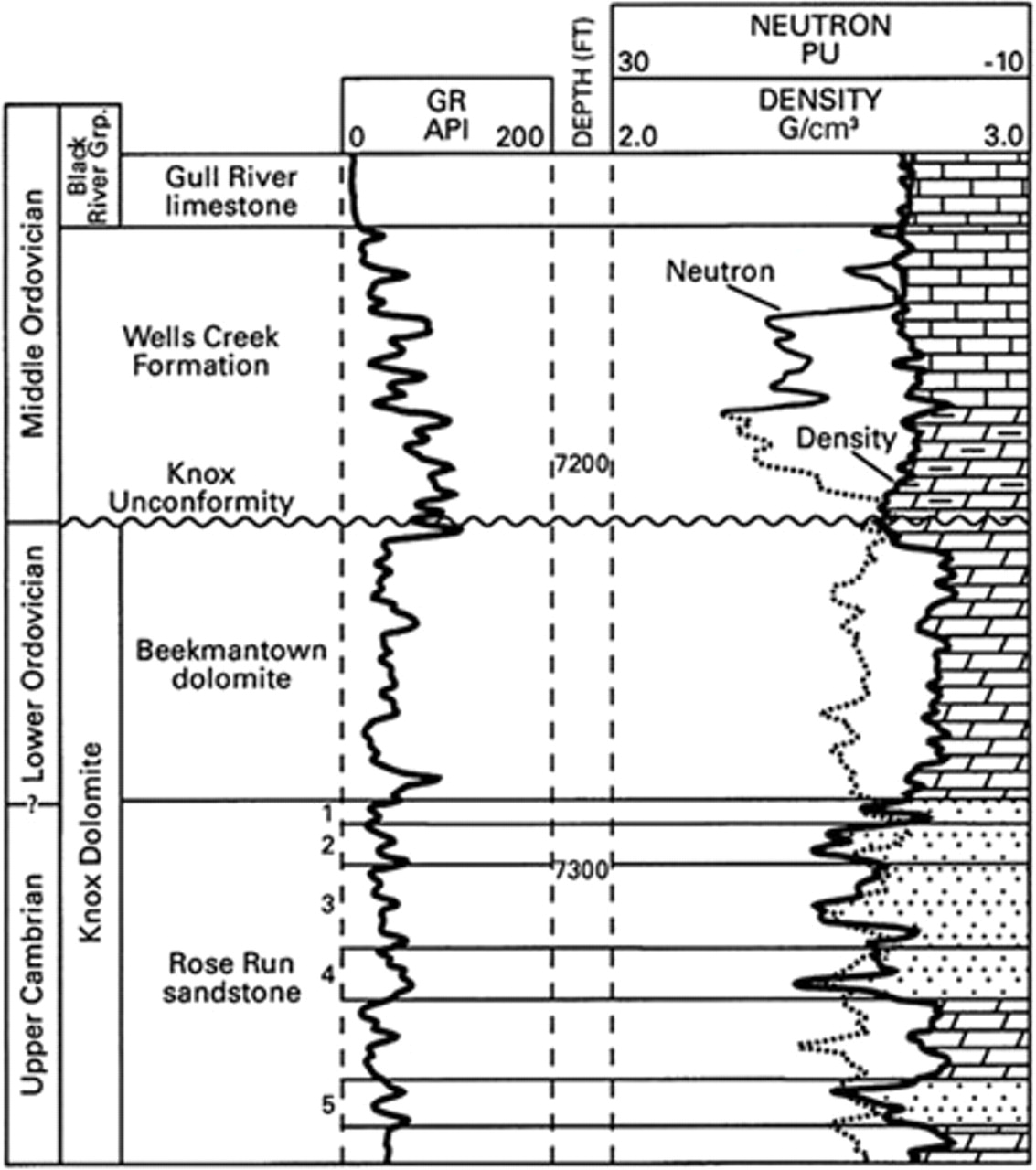

Last Friday Cabot Oil & Gas released its full year 2018 (and 4Q18) update, proclaiming 2018 was the best year ever for Cabot financially in the past almost 30 years the company has publicly traded shares of stock. The company hit new record natural gas production of 735 billion cubic feet equivalent (Bcfe) in 2018 (roughly 2 Bcfe/d), up 7% from 2017. Comments by Cabot Oil & Gas in their 2018 update issued Friday, along with added comments by CEO Dan Dinges during the earnings call on Friday, reveals the big news that Cabot has given up test drilling in Ohio Knox formation.

Comments by Cabot Oil & Gas in their 2018 update issued Friday, along with added comments by CEO Dan Dinges during the earnings call on Friday, reveals the big news that Cabot has given up test drilling in Ohio Knox formation. A startling revelation came from yesterday’s court hearing in the tiny village of Montrose, PA. Some of the landowners from Dimock, PA who have traveled around the country claiming their water had been contaminated by Cabot Oil & Gas (remember the fraud “documentary” called Gasland?) were actually paid up to $5,000 *per month* by green groups to spread their lies.

A startling revelation came from yesterday’s court hearing in the tiny village of Montrose, PA. Some of the landowners from Dimock, PA who have traveled around the country claiming their water had been contaminated by Cabot Oil & Gas (remember the fraud “documentary” called Gasland?) were actually paid up to $5,000 *per month* by green groups to spread their lies.

The evidence continues to pour in that the addition of Williams’ Atlantic Sunrise Pipeline, a 200-mile greenfield pipeline from northeastern to southeastern PA where it joins the Transco Pipeline, is having a dramatic and ongoing effect on natural gas prices in northeastern PA. As in, the price drillers get for their gas has doubled. Atlantic Sunrise went online in early October (see

The evidence continues to pour in that the addition of Williams’ Atlantic Sunrise Pipeline, a 200-mile greenfield pipeline from northeastern to southeastern PA where it joins the Transco Pipeline, is having a dramatic and ongoing effect on natural gas prices in northeastern PA. As in, the price drillers get for their gas has doubled. Atlantic Sunrise went online in early October (see  The expert analysts at RBN Energy have just published their “fourth and final” in a series of posts looking in detail at E&Ps (exploration & production companies, or “drillers”). One of the groups of E&Ps they examine are “gas-weighted” E&Ps–or drillers who mostly extract natural gas. In looking through the list, you immediately realize every one of them has operations in the Marcellus and/or Utica Shale region. Yes, a few also have operations in other plays, but they all have at least some operations here. The real value in the article is an accompanying spreadsheet comparing various financial metrics (apples to apples)–things like total revenue, lifting costs, production costs, and “pre-tax income,” meaning profitability. How do our drillers compare with each other?

The expert analysts at RBN Energy have just published their “fourth and final” in a series of posts looking in detail at E&Ps (exploration & production companies, or “drillers”). One of the groups of E&Ps they examine are “gas-weighted” E&Ps–or drillers who mostly extract natural gas. In looking through the list, you immediately realize every one of them has operations in the Marcellus and/or Utica Shale region. Yes, a few also have operations in other plays, but they all have at least some operations here. The real value in the article is an accompanying spreadsheet comparing various financial metrics (apples to apples)–things like total revenue, lifting costs, production costs, and “pre-tax income,” meaning profitability. How do our drillers compare with each other? Williams is expanding its mighty, 10,500-mile Transcontinental Gas Pipe Line Co (Transco), again. Sometime this month Williams will prefile a request with the Federal Energy Regulatory Commission for the Leidy South expansion project. The new project will bump up “compression” (either build new compressors or refit existing compressors) and build new “looping” pipeline in Pennsylvania, in order to increase capacity of Transco in the northeast Marcellus region by another 580 million cubic feet per day (MMcf/d).

Williams is expanding its mighty, 10,500-mile Transcontinental Gas Pipe Line Co (Transco), again. Sometime this month Williams will prefile a request with the Federal Energy Regulatory Commission for the Leidy South expansion project. The new project will bump up “compression” (either build new compressors or refit existing compressors) and build new “looping” pipeline in Pennsylvania, in order to increase capacity of Transco in the northeast Marcellus region by another 580 million cubic feet per day (MMcf/d).

Cabot Oil & Gas is drilling test wells in north central Ohio looking for “what’s next” after the Marcellus. So far Cabot, long known for its prolific production in the Marcellus Shale, has drilled two test wells and is in the process of permitting/drilling a third well, all in Ashland County, OH. Now Cabot is turning its sights on neighboring Richland County. Last Tuesday Cabot reps briefed Richland County commissioners on what they’re doing in Ashland County, and what they would like to do in Richland. Here’s the latest on Cabot’s effort to locate a new rock layer, hoping to spin straw into gold like they’ve done in Susquehanna County, PA…

Cabot Oil & Gas is drilling test wells in north central Ohio looking for “what’s next” after the Marcellus. So far Cabot, long known for its prolific production in the Marcellus Shale, has drilled two test wells and is in the process of permitting/drilling a third well, all in Ashland County, OH. Now Cabot is turning its sights on neighboring Richland County. Last Tuesday Cabot reps briefed Richland County commissioners on what they’re doing in Ashland County, and what they would like to do in Richland. Here’s the latest on Cabot’s effort to locate a new rock layer, hoping to spin straw into gold like they’ve done in Susquehanna County, PA… According to a report from BTU Analytics, the top three shippers who will soon flow natural gas along Williams’ Atlantic Sunrise Pipeline (ASP)–Cabot Oil & Gas, Seneca Resources and Chief Oil & Gas–have “nearly doubled” their rig counts over the past few months leading up to the imminent startup of ASP. The pipeline is due to go online any day now–by the end of August (see

According to a report from BTU Analytics, the top three shippers who will soon flow natural gas along Williams’ Atlantic Sunrise Pipeline (ASP)–Cabot Oil & Gas, Seneca Resources and Chief Oil & Gas–have “nearly doubled” their rig counts over the past few months leading up to the imminent startup of ASP. The pipeline is due to go online any day now–by the end of August (see