Arsenal Resources | Ascent Resources | Belmont County | Blackhill Energy | Bradford County | Energy Companies | EQT Corp | Expand Energy | Greene County (PA) | Guernsey County | Infinity Natural Resources | Monroe County | Ohio | Pennsylvania | Taylor County | Weekly Permits | West Virginia | Wetzel County

24 New Shale Well Permits Issued for PA-OH-WV Feb 2 – 8

The Marcellus/Utica region received a combined 24 new drilling permits last week, Feb. 2 – 8, up 2 from the permits issued two weeks ago. Pennsylvania issued 10 new permits, Ohio issued 10, and West Virginia issued 4. The drillers receiving new permits last week included: Arsenal Resources, Ascent Resources, Blackhill Energy, EQT, Expand Energy, and Infinity Natural Resources. Read More “24 New Shale Well Permits Issued for PA-OH-WV Feb 2 – 8”

The Marcellus/Utica region received a combined 24 new drilling permits last week, Feb. 2 – 8, up 2 from the permits issued two weeks ago. Pennsylvania issued 10 new permits, Ohio issued 10, and West Virginia issued 4. The drillers receiving new permits last week included: Arsenal Resources, Ascent Resources, Blackhill Energy, EQT, Expand Energy, and Infinity Natural Resources. Read More “24 New Shale Well Permits Issued for PA-OH-WV Feb 2 – 8”

Antero Resources, the largest Marcellus/Utica (M-U) driller in West Virginia, released its Q4 2025 update yesterday. In 2025, Antero Resources underwent a “transformational expansion” highlighted by the acquisition of HG Energy, the largest acquisition in Antero’s history, which the company closed on just last week (see

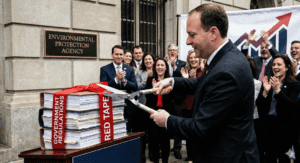

Antero Resources, the largest Marcellus/Utica (M-U) driller in West Virginia, released its Q4 2025 update yesterday. In 2025, Antero Resources underwent a “transformational expansion” highlighted by the acquisition of HG Energy, the largest acquisition in Antero’s history, which the company closed on just last week (see  President Donald Trump and EPA Administrator Lee Zeldin announced the “largest deregulatory action in American history” yesterday by officially revoking the Obama EPA’s 2009 “endangerment finding.” This move eliminates the legal mandate for the federal government to regulate greenhouse gases like carbon dioxide. The administration claims the rollback will save taxpayers over $1.3 trillion and reduce vehicle prices by approximately $2,400 by stripping away emission standards for cars and trucks. More importantly, it takes away the left’s ability to block coal- and natural gas-fired power plants. While Trump hailed the decision as a victory for consumer choice and the economy, anti-fossil fuel fanatics vowed to challenge the repeal in court.

President Donald Trump and EPA Administrator Lee Zeldin announced the “largest deregulatory action in American history” yesterday by officially revoking the Obama EPA’s 2009 “endangerment finding.” This move eliminates the legal mandate for the federal government to regulate greenhouse gases like carbon dioxide. The administration claims the rollback will save taxpayers over $1.3 trillion and reduce vehicle prices by approximately $2,400 by stripping away emission standards for cars and trucks. More importantly, it takes away the left’s ability to block coal- and natural gas-fired power plants. While Trump hailed the decision as a victory for consumer choice and the economy, anti-fossil fuel fanatics vowed to challenge the repeal in court.  Capital & Main is a left-leaning news outlet based in California. The publication has repeatedly targeted CNX Resources to smear the company and its Radical Transparency initiative. In September, we brought you Capital & Main’s latest hit piece alleging CNX’s operations are polluting and causing ill health for those who live nearby. The article also said CNX’s drilling program is anything but transparent (see

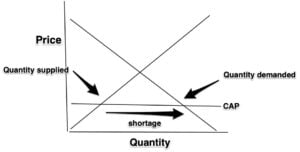

Capital & Main is a left-leaning news outlet based in California. The publication has repeatedly targeted CNX Resources to smear the company and its Radical Transparency initiative. In September, we brought you Capital & Main’s latest hit piece alleging CNX’s operations are polluting and causing ill health for those who live nearby. The article also said CNX’s drilling program is anything but transparent (see  PJM Interconnection, the electrical grid operator that covers Pennsylvania (along with all or parts of 12 other states and the District of Columbia), has once again caved to the political demands of PA Gov. Josh Shapiro to artificially cap prices in its upcoming capacity auctions for the next two years. PJM caved for the July 2025 auction (see

PJM Interconnection, the electrical grid operator that covers Pennsylvania (along with all or parts of 12 other states and the District of Columbia), has once again caved to the political demands of PA Gov. Josh Shapiro to artificially cap prices in its upcoming capacity auctions for the next two years. PJM caved for the July 2025 auction (see  The Canadian province of Quebec has significant natural gas potential in the Utica and Lorraine shale formations and on the Gaspé Peninsula, yet these resources remain untapped due to politics. The left has hoodwinked residents into believing hydraulic fracturing is from Satan and that it will pollute groundwater and cause earthquakes. Quebec became the first jurisdiction to permanently ban oil and gas exploration in 2022, prioritizing climate mythology over energy development. Consequently, the province imports nearly all its supplies from Western Canada and the United States. The province’s future strategy focuses on transitioning to renewable natural gas (which emits as much CO2 when burned as shale gas) and hydrogen, while maintaining a strict moratorium on local extraction.

The Canadian province of Quebec has significant natural gas potential in the Utica and Lorraine shale formations and on the Gaspé Peninsula, yet these resources remain untapped due to politics. The left has hoodwinked residents into believing hydraulic fracturing is from Satan and that it will pollute groundwater and cause earthquakes. Quebec became the first jurisdiction to permanently ban oil and gas exploration in 2022, prioritizing climate mythology over energy development. Consequently, the province imports nearly all its supplies from Western Canada and the United States. The province’s future strategy focuses on transitioning to renewable natural gas (which emits as much CO2 when burned as shale gas) and hydrogen, while maintaining a strict moratorium on local extraction.  MARCELLUS/UTICA REGION: Core Natural Resources bets on AI data center power demand surge; OTHER U.S. REGIONS: Virginia would be wise to remain out of RGGI; The Sunshine State is a heavyweight in natural gas consumption; NATIONAL: U.S. natural gas settles higher after storage miss; The Super Bowl without EVs tells you everything; Mom-and-pop shops remain the heart of the retail propane industry; Recognizing failure, some liberals are reshaping their climate messaging; INTERNATIONAL: Oil drops amid supply and equity jitters; Global exploration signaling ‘early recovery’; India will buy US LNG if offered at reasonable price, Petronet CEO says; Japanese oil and gas group Inpex sees LNG supply shortfall in Asia in 2035.

MARCELLUS/UTICA REGION: Core Natural Resources bets on AI data center power demand surge; OTHER U.S. REGIONS: Virginia would be wise to remain out of RGGI; The Sunshine State is a heavyweight in natural gas consumption; NATIONAL: U.S. natural gas settles higher after storage miss; The Super Bowl without EVs tells you everything; Mom-and-pop shops remain the heart of the retail propane industry; Recognizing failure, some liberals are reshaping their climate messaging; INTERNATIONAL: Oil drops amid supply and equity jitters; Global exploration signaling ‘early recovery’; India will buy US LNG if offered at reasonable price, Petronet CEO says; Japanese oil and gas group Inpex sees LNG supply shortfall in Asia in 2035.

Anti-fossil fuelers are raising concerns (and stoking fear with county residents) about a potential Duke Energy natural gas power plant in Davidson County, NC, after the project appeared in the company’s long-range planning documents. We first told you about this project three weeks ago (see

Anti-fossil fuelers are raising concerns (and stoking fear with county residents) about a potential Duke Energy natural gas power plant in Davidson County, NC, after the project appeared in the company’s long-range planning documents. We first told you about this project three weeks ago (see  Maryland State Senator Kevin Harris (D-Prince George’s) recently introduced legislation that would allow Big Utilities, such as Exelon, to build and operate power-generation infrastructure using ratepayer funds. The Alliance for Competitive Power (ACP) recently released a study that finds allowing Big Utilities to re-enter the powergen market in Maryland would shift financial risks and cost overruns to ratepayers, whereas competitive markets protect consumers by ensuring shareholders, not the public, bear investment risks. ACP argues that allowing Big Utilities to re-enter power generation would reduce competition and raise prices for ratepayers.

Maryland State Senator Kevin Harris (D-Prince George’s) recently introduced legislation that would allow Big Utilities, such as Exelon, to build and operate power-generation infrastructure using ratepayer funds. The Alliance for Competitive Power (ACP) recently released a study that finds allowing Big Utilities to re-enter the powergen market in Maryland would shift financial risks and cost overruns to ratepayers, whereas competitive markets protect consumers by ensuring shareholders, not the public, bear investment risks. ACP argues that allowing Big Utilities to re-enter power generation would reduce competition and raise prices for ratepayers.  Virginia Senate Bill 253, introduced by State Senator Louise Lucas (D-Portsmouth), aims to shift energy infrastructure costs from residents to data centers, potentially saving households a whopping $65 annually. The legislation requires data centers—which account for 20% of Dominion Energy’s sales—to fund their own electrical substations and cover specific “capacity costs.” If the bill becomes law and the proposals in it receive approval from the State Corporation Commission (SCC), the typical monthly energy bill for data centers would rise by about 16%, while the typical bill for residential and other customers would decrease by 3% to 3.5%. Looks like Virginia, with more data centers than any other state in the union, is now closed for data center business. Too bad.

Virginia Senate Bill 253, introduced by State Senator Louise Lucas (D-Portsmouth), aims to shift energy infrastructure costs from residents to data centers, potentially saving households a whopping $65 annually. The legislation requires data centers—which account for 20% of Dominion Energy’s sales—to fund their own electrical substations and cover specific “capacity costs.” If the bill becomes law and the proposals in it receive approval from the State Corporation Commission (SCC), the typical monthly energy bill for data centers would rise by about 16%, while the typical bill for residential and other customers would decrease by 3% to 3.5%. Looks like Virginia, with more data centers than any other state in the union, is now closed for data center business. Too bad.  Despite record-breaking domestic production, U.S. manufacturers increasingly face gas shortages and price spikes during extreme weather. While the shale boom promised cheap energy, insufficient pipeline infrastructure prioritizes residential heating, power plants, and long-term export contracts over industrial users. This disparity forced companies like Evonik and International Paper to halt production or pay exorbitant spot prices during recent winter storms. Consequently, manufacturing trade groups are urging federal regulators to reform pipeline contracting and prioritize domestic supply over exports.

Despite record-breaking domestic production, U.S. manufacturers increasingly face gas shortages and price spikes during extreme weather. While the shale boom promised cheap energy, insufficient pipeline infrastructure prioritizes residential heating, power plants, and long-term export contracts over industrial users. This disparity forced companies like Evonik and International Paper to halt production or pay exorbitant spot prices during recent winter storms. Consequently, manufacturing trade groups are urging federal regulators to reform pipeline contracting and prioritize domestic supply over exports.  The U.S. Energy Information Administration (EIA) issued its latest monthly Short-Term Energy Outlook (STEO) yesterday. The STEO is the agency’s monthly best estimate of where energy prices and production will head over the next 12 months. There was a major revision to the agency’s prediction about the spot price (at the Henry Hub) for natural gas in 2026. Just last month, EIA predicted the HH spot price would average $3.46 per million British thermal units (see

The U.S. Energy Information Administration (EIA) issued its latest monthly Short-Term Energy Outlook (STEO) yesterday. The STEO is the agency’s monthly best estimate of where energy prices and production will head over the next 12 months. There was a major revision to the agency’s prediction about the spot price (at the Henry Hub) for natural gas in 2026. Just last month, EIA predicted the HH spot price would average $3.46 per million British thermal units (see  Duke Energy, headquartered in Charlotte, N.C., is one of the largest U.S. energy holding companies, serving 8.7 million electric customers and 1.8 million gas customers across six states as of early 2026. While the company dabbles in unreliable renewables like solar and wind, its bread-and-butter, go-to source for new electric power generation is natural gas, which it gets from the Marcellus/Utica. We’ve reported on many of Duke’s announced new gas-fired power plant projects (

Duke Energy, headquartered in Charlotte, N.C., is one of the largest U.S. energy holding companies, serving 8.7 million electric customers and 1.8 million gas customers across six states as of early 2026. While the company dabbles in unreliable renewables like solar and wind, its bread-and-butter, go-to source for new electric power generation is natural gas, which it gets from the Marcellus/Utica. We’ve reported on many of Duke’s announced new gas-fired power plant projects (