Physicist Debunks the “Too Much CO2 in the Atmosphere” Argument

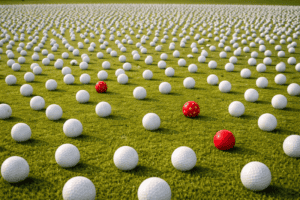

Dr. Kelvin Kemm is a South African nuclear physicist and past Chairman of the South African Nuclear Energy Corporation (Necsa). In an article on the Committee For A Constructive Tomorrow (CFACT) website, Kemm highlights a political exchange in which Senator John Kennedy exposed a climate advocate’s lack of knowledge about atmospheric CO2 concentrations. Kemm clarifies that CO2 levels are merely 0.04% of the Earth’s atmosphere, illustrating this with a 10,000-golf-ball analogy in which only one “yellow-dotted” ball represents human-added emissions since the 1860s. Read More “Physicist Debunks the “Too Much CO2 in the Atmosphere” Argument”

Dr. Kelvin Kemm is a South African nuclear physicist and past Chairman of the South African Nuclear Energy Corporation (Necsa). In an article on the Committee For A Constructive Tomorrow (CFACT) website, Kemm highlights a political exchange in which Senator John Kennedy exposed a climate advocate’s lack of knowledge about atmospheric CO2 concentrations. Kemm clarifies that CO2 levels are merely 0.04% of the Earth’s atmosphere, illustrating this with a 10,000-golf-ball analogy in which only one “yellow-dotted” ball represents human-added emissions since the 1860s. Read More “Physicist Debunks the “Too Much CO2 in the Atmosphere” Argument”

Last April, Knighthead Capital Management, Homer City Redevelopment (HCR), and Kiewit Power Constructors Co. announced a plan to convert the former Homer City Generating Station, previously the largest coal-fired power plant in Pennsylvania (Indiana County, 50 miles east of Pittsburgh) into a more than 3,200-acre natural gas-powered data center campus, designed to meet the growing demand for artificial intelligence (AI) and high-performance computing (see

Last April, Knighthead Capital Management, Homer City Redevelopment (HCR), and Kiewit Power Constructors Co. announced a plan to convert the former Homer City Generating Station, previously the largest coal-fired power plant in Pennsylvania (Indiana County, 50 miles east of Pittsburgh) into a more than 3,200-acre natural gas-powered data center campus, designed to meet the growing demand for artificial intelligence (AI) and high-performance computing (see  One of the great ironies of the Marcellus Shale is that THE TOP two natgas-producing counties in the state, Susquehanna (#1) and Bradford (#2), both of which are rural, don’t, for the most part, offer the gas extracted from under their residents to their residents for everyday use. It costs a lot of money to run local distribution pipelines to homes and businesses for natural gas. Leatherstocking Gas Company is on a mission to change that. Leatherstocking provides natural gas utility service in Susquehanna and Bradford to some 500+ customers. More customers will soon be added to Leatherstocking’s service in Wyalusing (Bradford County) following a recent PIPE grant.

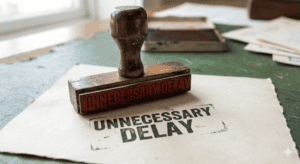

One of the great ironies of the Marcellus Shale is that THE TOP two natgas-producing counties in the state, Susquehanna (#1) and Bradford (#2), both of which are rural, don’t, for the most part, offer the gas extracted from under their residents to their residents for everyday use. It costs a lot of money to run local distribution pipelines to homes and businesses for natural gas. Leatherstocking Gas Company is on a mission to change that. Leatherstocking provides natural gas utility service in Susquehanna and Bradford to some 500+ customers. More customers will soon be added to Leatherstocking’s service in Wyalusing (Bradford County) following a recent PIPE grant.  Connecticut’s Department of Energy and Environmental Protection (DEEP) has determined that Eversource Energy’s plan to install a natural gas pipeline through Hurd State Park and the Connecticut Valley Railroad State Park Trail requires a formal Environmental Impact Evaluation, unnecessarily delaying a tiny portion (1.1 miles) of a critically-important reliability project (34.5 miles long). This 16-inch pipeline, a segment of the Southeast Resiliency Project, is designed to provide energy redundancy and security for the region.

Connecticut’s Department of Energy and Environmental Protection (DEEP) has determined that Eversource Energy’s plan to install a natural gas pipeline through Hurd State Park and the Connecticut Valley Railroad State Park Trail requires a formal Environmental Impact Evaluation, unnecessarily delaying a tiny portion (1.1 miles) of a critically-important reliability project (34.5 miles long). This 16-inch pipeline, a segment of the Southeast Resiliency Project, is designed to provide energy redundancy and security for the region.  The province of Québec, Canada, with a huge supply of Utica Shale gas sitting beneath it, passed a new law in 2022 outlawing all oil and natural gas production throughout the province, called Bill 21 (see

The province of Québec, Canada, with a huge supply of Utica Shale gas sitting beneath it, passed a new law in 2022 outlawing all oil and natural gas production throughout the province, called Bill 21 (see  Yesterday, the Trump administration announced “South Mon,” a $17 billion natural gas-fueled facility in southwestern Pennsylvania intended to expand domestic energy production. Part of a $550 billion trade deal with Japan, the hub will be operated by NextEra Energy Resources and generate 4.3 gigawatts (GW) of power. By tapping into the Marcellus and Utica shale regions and connecting to the PJM regional transmission network, the project aims to meet rising demand, lower energy costs, and create local jobs. South Mon is one of three major energy hubs planned nationwide to enhance power affordability and infrastructure across the Mid-Atlantic market.

Yesterday, the Trump administration announced “South Mon,” a $17 billion natural gas-fueled facility in southwestern Pennsylvania intended to expand domestic energy production. Part of a $550 billion trade deal with Japan, the hub will be operated by NextEra Energy Resources and generate 4.3 gigawatts (GW) of power. By tapping into the Marcellus and Utica shale regions and connecting to the PJM regional transmission network, the project aims to meet rising demand, lower energy costs, and create local jobs. South Mon is one of three major energy hubs planned nationwide to enhance power affordability and infrastructure across the Mid-Atlantic market.  Eastern Shore developer TeraWulf has reached a deal to acquire the retired Morgantown Generating Station in Charles County (on the Potomac River), proposing to transform the site into a massive natural gas-powered data center campus. The plan aims to generate one gigawatt (GW) of power and 500 megawatts of battery storage, bypassing the aging regional grid. While TeraWulf claims support from Governor Wes Moore’s administration, the project faces intense scrutiny from environmental groups and local residents concerned about fossil fuel emissions and transparency. Critics also question the financial stability of the cryptocurrency-focused firm, though company leadership maintains they have the expertise to remediate the site.

Eastern Shore developer TeraWulf has reached a deal to acquire the retired Morgantown Generating Station in Charles County (on the Potomac River), proposing to transform the site into a massive natural gas-powered data center campus. The plan aims to generate one gigawatt (GW) of power and 500 megawatts of battery storage, bypassing the aging regional grid. While TeraWulf claims support from Governor Wes Moore’s administration, the project faces intense scrutiny from environmental groups and local residents concerned about fossil fuel emissions and transparency. Critics also question the financial stability of the cryptocurrency-focused firm, though company leadership maintains they have the expertise to remediate the site.  This is one of those “man bites dog” stories. When was the last time you heard about Democrat state legislators from one of the bluest of blue states voting to roll back funding for “green” programs in order to save money? Yeah, like NEVER. At least, until now. Funny how even Dems will throw their precious green philosophies out the window if their job (getting reelected) is on the line. That’s what is happening in Maryland.

This is one of those “man bites dog” stories. When was the last time you heard about Democrat state legislators from one of the bluest of blue states voting to roll back funding for “green” programs in order to save money? Yeah, like NEVER. At least, until now. Funny how even Dems will throw their precious green philosophies out the window if their job (getting reelected) is on the line. That’s what is happening in Maryland.  No one should be surprised that far-left Democrat Josh Shapiro, currently the Governor of Pennsylvania (but with a major passion to become President), joined his fellow radicals from other blue states in launching a lawsuit against the Trump administration for moving to eliminate the extremist “endangerment finding” concocted by Lord Obama and the Obamadroids of the EPA. Trump’s move to overturn the finding will save Americans roughly $3,800 each. Yet Shapiro and his fellow cabal members want to keep Americans poor and subservient (to them).

No one should be surprised that far-left Democrat Josh Shapiro, currently the Governor of Pennsylvania (but with a major passion to become President), joined his fellow radicals from other blue states in launching a lawsuit against the Trump administration for moving to eliminate the extremist “endangerment finding” concocted by Lord Obama and the Obamadroids of the EPA. Trump’s move to overturn the finding will save Americans roughly $3,800 each. Yet Shapiro and his fellow cabal members want to keep Americans poor and subservient (to them).  Here we go again: another rebranding of ESG and another attempt to brand natural gas as low-emissions, clean, and green. Pipeline giant Williams has launched what it calls its NextGen Gas program to offer “verified lower-emissions natural gas from wellhead to market.” NextGen Gas measures methane and carbon dioxide equivalent (CO2e) emissions intensity from wellhead to market, increasing transparency into how natural gas is produced and delivered along a specific gas pathway.

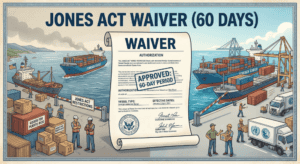

Here we go again: another rebranding of ESG and another attempt to brand natural gas as low-emissions, clean, and green. Pipeline giant Williams has launched what it calls its NextGen Gas program to offer “verified lower-emissions natural gas from wellhead to market.” NextGen Gas measures methane and carbon dioxide equivalent (CO2e) emissions intensity from wellhead to market, increasing transparency into how natural gas is produced and delivered along a specific gas pathway.  We lead with this story about a government regulatory action because of just how important we see this development. For *years* we have railed against the 106-year-old Jones Act and its requirement that any goods (like LNG) that are transported from one U.S. port to another be on a ship manufactured in the U.S., owned by a U.S. company, and crewed by a U.S. crew. The effect of this law in the modern age is to ban LNG (and other shipments, like gasoline, propane, coal, and other products manufactured in the U.S.) from being shipped cheaply from port to port. The U.S. foolishly allowed its ship manufacturing to slip away years ago to South Korea and other countries. We no longer make cargo carriers for LNG and other energy products. We haven’t made them in decades. Yesterday, President Trump signed a 60-day waiver of the Jones Act, allowing certain goods (such as LNG, fertilizer, and coal) to be transported from U.S. port to U.S. port on foreign-owned, foreign-flagged and crewed ships.

We lead with this story about a government regulatory action because of just how important we see this development. For *years* we have railed against the 106-year-old Jones Act and its requirement that any goods (like LNG) that are transported from one U.S. port to another be on a ship manufactured in the U.S., owned by a U.S. company, and crewed by a U.S. crew. The effect of this law in the modern age is to ban LNG (and other shipments, like gasoline, propane, coal, and other products manufactured in the U.S.) from being shipped cheaply from port to port. The U.S. foolishly allowed its ship manufacturing to slip away years ago to South Korea and other countries. We no longer make cargo carriers for LNG and other energy products. We haven’t made them in decades. Yesterday, President Trump signed a 60-day waiver of the Jones Act, allowing certain goods (such as LNG, fertilizer, and coal) to be transported from U.S. port to U.S. port on foreign-owned, foreign-flagged and crewed ships.  Just coming to light for us now is that Iroquois Gas Transmission System petitioned the Federal Energy Regulatory Commission (FERC) in February to reissue authorization for the $152 million Wright Interconnect Project in New York State, aiming to revive a critical link for the previously canceled Constitution Pipeline. Originally approved in 2014, the project seeks to establish a new receipt interconnection and compression facilities at the Wright Compressor Station. By creating 650,000 dekatherms per day (650 MMcf/d) of transportation capacity, the initiative intends to alleviate persistent natural gas supply constraints in the Northeast and New England markets. If approved, the project targets a May 2028 in-service date, utilizing existing company-owned infrastructure to minimize environmental impacts.

Just coming to light for us now is that Iroquois Gas Transmission System petitioned the Federal Energy Regulatory Commission (FERC) in February to reissue authorization for the $152 million Wright Interconnect Project in New York State, aiming to revive a critical link for the previously canceled Constitution Pipeline. Originally approved in 2014, the project seeks to establish a new receipt interconnection and compression facilities at the Wright Compressor Station. By creating 650,000 dekatherms per day (650 MMcf/d) of transportation capacity, the initiative intends to alleviate persistent natural gas supply constraints in the Northeast and New England markets. If approved, the project targets a May 2028 in-service date, utilizing existing company-owned infrastructure to minimize environmental impacts.  The tagline (remit) of Marcellus Drilling News is “Helping People & Businesses Profit from Northeast Shale Drilling.” Sometimes people can make money apart from leasing land and drilling. As we have pointed out many times, there is a direct connection between shale gas and the power generation market. Gas-fired power plants use (are HUGE customers for) natural gas extracted in the Marcellus and the Utica. AI data centers, which have burst on the scene over the past year or so, have an enormous appetite for electricity. Most of the electricity used to power data centers comes from gas-fired power plants, whether those plants are owned and operated by independent power operators, or (increasingly) owned and operated on-site by the data center itself. This is the story of one farmer in northeastern Pennsylvania who became a millionaire apart from shale drilling—by selling his small farm to a data center company.

The tagline (remit) of Marcellus Drilling News is “Helping People & Businesses Profit from Northeast Shale Drilling.” Sometimes people can make money apart from leasing land and drilling. As we have pointed out many times, there is a direct connection between shale gas and the power generation market. Gas-fired power plants use (are HUGE customers for) natural gas extracted in the Marcellus and the Utica. AI data centers, which have burst on the scene over the past year or so, have an enormous appetite for electricity. Most of the electricity used to power data centers comes from gas-fired power plants, whether those plants are owned and operated by independent power operators, or (increasingly) owned and operated on-site by the data center itself. This is the story of one farmer in northeastern Pennsylvania who became a millionaire apart from shale drilling—by selling his small farm to a data center company.  The Natural Gas Pipeline Company of America (NGPL), a Kinder Morgan pipeline subsidiary, flows Marcellus and Utica molecules. While the pipeline’s primary footprint is in the Midcontinent and Gulf Coast, it is a critical takeaway path for Appalachian gas through key interconnections. NGPL’s recent tariff announcement reaffirmed its commitment to offering negotiated rate arrangements for pipeline transportation services, maintaining continuity in its commercial practices. These options allow shippers to develop customized pricing based on factors like contract duration, gas volume, and specific operating needs, providing greater flexibility than standard maximum recourse rates.

The Natural Gas Pipeline Company of America (NGPL), a Kinder Morgan pipeline subsidiary, flows Marcellus and Utica molecules. While the pipeline’s primary footprint is in the Midcontinent and Gulf Coast, it is a critical takeaway path for Appalachian gas through key interconnections. NGPL’s recent tariff announcement reaffirmed its commitment to offering negotiated rate arrangements for pipeline transportation services, maintaining continuity in its commercial practices. These options allow shippers to develop customized pricing based on factors like contract duration, gas volume, and specific operating needs, providing greater flexibility than standard maximum recourse rates.  In January, Constellation Energy Corporation finalized its acquisition of Calpine Corporation, becoming the largest private-sector electricity producer in the United States (see

In January, Constellation Energy Corporation finalized its acquisition of Calpine Corporation, becoming the largest private-sector electricity producer in the United States (see