SRBC Approved 76 Shale Gas Well Pad Water Use Permits in Sep/Oct

The highly functional and responsible Susquehanna River Basin Commission (SRBC), unlike its highly dysfunctional and irresponsible counterpart, the Delaware River Basin Commission (DRBC), continues to support the shale energy industry by approving water withdrawals and consumptive use requests for responsible and safe shale drilling. The SRBC published a notice in the December 6 Pennsylvania Bulletin that the Executive Director of the SRBC approved and/or renewed 76 general water use permits from September 1 through October 31 for individual shale gas well drilling pads in Blair, Bradford, Cameron, Centre, Clearfield, Clinton, Elk, Huntingdon, Lycoming, McKean, Sullivan, Susquehanna and Tioga counties in Pennsylvania and one permit to withdraw water in Steuben County, New York. Read More “SRBC Approved 76 Shale Gas Well Pad Water Use Permits in Sep/Oct”

The highly functional and responsible Susquehanna River Basin Commission (SRBC), unlike its highly dysfunctional and irresponsible counterpart, the Delaware River Basin Commission (DRBC), continues to support the shale energy industry by approving water withdrawals and consumptive use requests for responsible and safe shale drilling. The SRBC published a notice in the December 6 Pennsylvania Bulletin that the Executive Director of the SRBC approved and/or renewed 76 general water use permits from September 1 through October 31 for individual shale gas well drilling pads in Blair, Bradford, Cameron, Centre, Clearfield, Clinton, Elk, Huntingdon, Lycoming, McKean, Sullivan, Susquehanna and Tioga counties in Pennsylvania and one permit to withdraw water in Steuben County, New York. Read More “SRBC Approved 76 Shale Gas Well Pad Water Use Permits in Sep/Oct”

In January, Constellation Energy (a huge power-generating company) announced a deal to buy out and merge with Calpine (another huge power-generating company). Calpine owns 79 energy facilities across the country, generating some 27 gigawatts (GW) of electricity, with a significant number located in the eastern U.S. Many of Calpine’s facilities use natural gas to produce electricity. The two companies combined would own almost 60 GW of nuclear, natural gas, geothermal, hydro, wind, solar, cogeneration, and battery storage. The Federal Energy Regulatory Commission (FERC) signed off on the deal in July, with conditions (see

In January, Constellation Energy (a huge power-generating company) announced a deal to buy out and merge with Calpine (another huge power-generating company). Calpine owns 79 energy facilities across the country, generating some 27 gigawatts (GW) of electricity, with a significant number located in the eastern U.S. Many of Calpine’s facilities use natural gas to produce electricity. The two companies combined would own almost 60 GW of nuclear, natural gas, geothermal, hydro, wind, solar, cogeneration, and battery storage. The Federal Energy Regulatory Commission (FERC) signed off on the deal in July, with conditions (see  Last week, the Baker Hughes U.S. national rig count recovered some of the previous week’s losses. The count increased by five after losing 10 rigs in the previous week. The national count went from 544 to 549. Rigs in the Marcellus/Utica remained the same last week—now for three weeks in a row. Pennsylvania has held at 18 for three consecutive weeks. Ohio was the same at 13 rigs, which it has operated since September 26. West Virginia maintained its 7 rigs, which it has operated since May 30. There were 24 rigs targeting the Marcellus and 14 targeting the Utica, for a combined 38 rigs in the M-U.

Last week, the Baker Hughes U.S. national rig count recovered some of the previous week’s losses. The count increased by five after losing 10 rigs in the previous week. The national count went from 544 to 549. Rigs in the Marcellus/Utica remained the same last week—now for three weeks in a row. Pennsylvania has held at 18 for three consecutive weeks. Ohio was the same at 13 rigs, which it has operated since September 26. West Virginia maintained its 7 rigs, which it has operated since May 30. There were 24 rigs targeting the Marcellus and 14 targeting the Utica, for a combined 38 rigs in the M-U.  OTHER U.S. REGIONS: Bowman buys RPT to boost data center power engineering; Newsom’s California slouching towards a self-inflicted energy crisis; NATIONAL: Natural gas surge 9% this week on strong flow of exports; MAHA activists urge Trump to fire his E.P.A. Administrator; Green energy’s problems go beyond messaging; Climate rift opens between Amazon and rivals in row over data centre power; Halliburton promotes Slocum to COO role; WoodMac flags ‘key themes’ shaping lower 48 in 2026; U.S. retail gasoline prices fall below $3 per gallon, the lowest since 2021; INTERNATIONAL: Crude finishes higher on short covering; Today’s $67 per barrel is only $44 in 2008 dollars; Rationality returns to Australia as climate scare wanes; China’s paradox – kingdom of solar, wind, hydro, nuclear and coal.

OTHER U.S. REGIONS: Bowman buys RPT to boost data center power engineering; Newsom’s California slouching towards a self-inflicted energy crisis; NATIONAL: Natural gas surge 9% this week on strong flow of exports; MAHA activists urge Trump to fire his E.P.A. Administrator; Green energy’s problems go beyond messaging; Climate rift opens between Amazon and rivals in row over data centre power; Halliburton promotes Slocum to COO role; WoodMac flags ‘key themes’ shaping lower 48 in 2026; U.S. retail gasoline prices fall below $3 per gallon, the lowest since 2021; INTERNATIONAL: Crude finishes higher on short covering; Today’s $67 per barrel is only $44 in 2008 dollars; Rationality returns to Australia as climate scare wanes; China’s paradox – kingdom of solar, wind, hydro, nuclear and coal.

In Q3 2025, U.S. E&Ps (drillers) successfully leveraged rigorous cost-cutting and capital discipline to maintain stable earnings despite commodity price volatility. With lifting costs down 16% since mid-2022, producers offset revenue pressures through efficiency and consolidation. RBN Energy reports that performance diverged by sector in 3Q: oil-weighted producers saw earnings rise 19% on stabilized crude prices and reduced impairments, while gas-weighted peers suffered a 27% earnings slump due to lower realizations. Total production increased 4.7%, mainly driven by oil majors. Looking ahead to Q4, the outlook shifts; oil producers face headwinds as prices dip toward $60/bbl, while natural gas producers anticipate a strong finish fueled by winter demand and rising Henry Hub prices.

In Q3 2025, U.S. E&Ps (drillers) successfully leveraged rigorous cost-cutting and capital discipline to maintain stable earnings despite commodity price volatility. With lifting costs down 16% since mid-2022, producers offset revenue pressures through efficiency and consolidation. RBN Energy reports that performance diverged by sector in 3Q: oil-weighted producers saw earnings rise 19% on stabilized crude prices and reduced impairments, while gas-weighted peers suffered a 27% earnings slump due to lower realizations. Total production increased 4.7%, mainly driven by oil majors. Looking ahead to Q4, the outlook shifts; oil producers face headwinds as prices dip toward $60/bbl, while natural gas producers anticipate a strong finish fueled by winter demand and rising Henry Hub prices.  Here we go again. The environmental left is attacking the shale industry by accusing it of shipping drill cuttings (the leftover rock and dirt that comes out of a borehole) to local landfills in the Buckeye State (Ohio), where it will irradiate everyone and everything close to it. According to the left, drill cuttings “could be contaminated with radioactivity and other chemicals.” And, according to the same people, lack of regulations in Ohio “allows it [radioactive drill cuttings] to slip by regulators, especially in Ohio,” and end up in the same landfills as “household trash.” Is there anything to the claim that drill cuttings are radioactive and a threat to those who live near landfills?

Here we go again. The environmental left is attacking the shale industry by accusing it of shipping drill cuttings (the leftover rock and dirt that comes out of a borehole) to local landfills in the Buckeye State (Ohio), where it will irradiate everyone and everything close to it. According to the left, drill cuttings “could be contaminated with radioactivity and other chemicals.” And, according to the same people, lack of regulations in Ohio “allows it [radioactive drill cuttings] to slip by regulators, especially in Ohio,” and end up in the same landfills as “household trash.” Is there anything to the claim that drill cuttings are radioactive and a threat to those who live near landfills?  In October 2024, the Bidenistas announced seven hydrogen hub projects (from 33 finalists) that would receive a collective $7 billion in federal funding (see

In October 2024, the Bidenistas announced seven hydrogen hub projects (from 33 finalists) that would receive a collective $7 billion in federal funding (see  A commentator writing for Reuters warns that soaring U.S. natural gas prices and falling global values are squeezing profit margins for American LNG exporters, threatening future exports. The narrowing price gap between U.S. and European markets, driven by high domestic demand and global oversupply, has reached its lowest point since 2021. The prognosticator postulates that while immediate production cuts are unlikely, a surge in new global capacity by 2027 could force reductions in U.S. LNG exports. Furthermore, rising domestic prices pose a political challenge for President Trump, as his promise to lower consumer energy costs conflicts with market tightening driven by increased LNG exports and energy-intensive data centers.

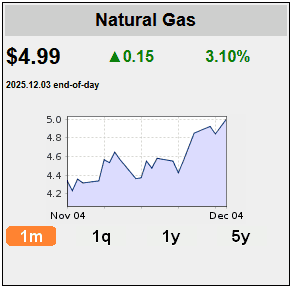

A commentator writing for Reuters warns that soaring U.S. natural gas prices and falling global values are squeezing profit margins for American LNG exporters, threatening future exports. The narrowing price gap between U.S. and European markets, driven by high domestic demand and global oversupply, has reached its lowest point since 2021. The prognosticator postulates that while immediate production cuts are unlikely, a surge in new global capacity by 2027 could force reductions in U.S. LNG exports. Furthermore, rising domestic prices pose a political challenge for President Trump, as his promise to lower consumer energy costs conflicts with market tightening driven by increased LNG exports and energy-intensive data centers.  Yesterday, the NYMEX “front-month” futures price for natural gas closed up 15 cents at $4.995 (call it $5), which is the highest closing price for NYMEX in nearly three years (since Dec. 27, 2022). Intraday trading of the front-month contract floated above $5 at points. Weather forecasts of impending frigid weather were the main reason for the increase. Futures prices are now up more than 60% compared with a year ago. “Forecasts for the coldest December since 2010 may tip storage into a deficit by Christmas,” trading firm EBW Analytics wrote in a note to clients. Fewer molecules with more demand equals higher prices. As for the spot price at trading hubs in the Marcellus/Utica region, averaging all of them together, the price closed yesterday at $4.74, nearly at parity with the Henry Hub spot price of $4.87. That’s unheard of!

Yesterday, the NYMEX “front-month” futures price for natural gas closed up 15 cents at $4.995 (call it $5), which is the highest closing price for NYMEX in nearly three years (since Dec. 27, 2022). Intraday trading of the front-month contract floated above $5 at points. Weather forecasts of impending frigid weather were the main reason for the increase. Futures prices are now up more than 60% compared with a year ago. “Forecasts for the coldest December since 2010 may tip storage into a deficit by Christmas,” trading firm EBW Analytics wrote in a note to clients. Fewer molecules with more demand equals higher prices. As for the spot price at trading hubs in the Marcellus/Utica region, averaging all of them together, the price closed yesterday at $4.74, nearly at parity with the Henry Hub spot price of $4.87. That’s unheard of!  Yesterday, the Pennsylvania Independent Fiscal Office (IFO) released its latest quarterly Natural Gas Production Report for July through September 2025 (full copy below). There were 116 new horizontal wells spud (drilled) in 3Q25, a huge increase of 53 wells (+84%) compared to 3Q24. Natural gas production volume was 1,934 billion cubic feet (Bcf) in 3Q25, up 93 Bcf (+5%) from 1,841 Bcf produced in 3Q24. The average Pennsylvania spot hub price was $2.18, an increase of $0.74 (+51%) from the prior year’s $1.44. All in all, it was a great third quarter for the PA Marcellus. The numbers are going in the right direction.

Yesterday, the Pennsylvania Independent Fiscal Office (IFO) released its latest quarterly Natural Gas Production Report for July through September 2025 (full copy below). There were 116 new horizontal wells spud (drilled) in 3Q25, a huge increase of 53 wells (+84%) compared to 3Q24. Natural gas production volume was 1,934 billion cubic feet (Bcf) in 3Q25, up 93 Bcf (+5%) from 1,841 Bcf produced in 3Q24. The average Pennsylvania spot hub price was $2.18, an increase of $0.74 (+51%) from the prior year’s $1.44. All in all, it was a great third quarter for the PA Marcellus. The numbers are going in the right direction.  Wondering how your business can profit from the Marcellus/Utica with production and drilling on the increase once again? A

Wondering how your business can profit from the Marcellus/Utica with production and drilling on the increase once again? A  Three anti-shale drilling groups—the PA Council of Trout Unlimited, the Keystone Trails Association, and the Responsible Drilling Alliance—have requested the Pennsylvania Department of Environmental Protection (DEP) hold a hearing on the Chapter 105 permit requested for a 3.9-mile shale gas access road and staging area proposed by PA General Energy in Gamble and Cascade Townships, Lycoming County. The aim of their request is not to elicit information or express concerns that can be addressed to achieve a better outcome; rather, it is to flood the hearing with bombastic charges in hopes of blocking the project altogether.

Three anti-shale drilling groups—the PA Council of Trout Unlimited, the Keystone Trails Association, and the Responsible Drilling Alliance—have requested the Pennsylvania Department of Environmental Protection (DEP) hold a hearing on the Chapter 105 permit requested for a 3.9-mile shale gas access road and staging area proposed by PA General Energy in Gamble and Cascade Townships, Lycoming County. The aim of their request is not to elicit information or express concerns that can be addressed to achieve a better outcome; rather, it is to flood the hearing with bombastic charges in hopes of blocking the project altogether.  There have been a number of new reports recently released predicting how new AI data center projects will affect (a) demand for electric power, and (b) demand for natural gas to generate that power. We spotted what at first glance appears to be contradictory predictions in two new reports issued this week. On Monday, BloombergNEF (the research arm of Bloomberg) issued a report predicting data center power demand will hit 106 gigawatts (GW) by 2035, a 36% jump from its previous outlook. Two days later, Enverus Intelligence® Research (EIR), a subsidiary of Enverus, issued a report that predicts 30 GW of new U.S. data center capacity will be needed over the next five years (by 2030)—significantly below the 50 GW forecasted by major grid operators. One report is wildly optimistic, the other pessimistic. What gives?

There have been a number of new reports recently released predicting how new AI data center projects will affect (a) demand for electric power, and (b) demand for natural gas to generate that power. We spotted what at first glance appears to be contradictory predictions in two new reports issued this week. On Monday, BloombergNEF (the research arm of Bloomberg) issued a report predicting data center power demand will hit 106 gigawatts (GW) by 2035, a 36% jump from its previous outlook. Two days later, Enverus Intelligence® Research (EIR), a subsidiary of Enverus, issued a report that predicts 30 GW of new U.S. data center capacity will be needed over the next five years (by 2030)—significantly below the 50 GW forecasted by major grid operators. One report is wildly optimistic, the other pessimistic. What gives?