KM Puts Elba Island Train #10 into Service – One Train Remains

The Federal Energy Regulatory Commission (FERC) granted permission to Kinder Morgan to begin service on train #10 at KM’s Elba Island LNG export facility, located near Savannah, Georgia. KM’s Elba project consists of 10 mini-trains, each capable of liquefying 0.3 million tonnes per annum (MTPA) of LNG–or roughly 40 million cubic feet per day (MMcf/d) of natural gas. There’s just one train left to bring online…

The Federal Energy Regulatory Commission (FERC) granted permission to Kinder Morgan to begin service on train #10 at KM’s Elba Island LNG export facility, located near Savannah, Georgia. KM’s Elba project consists of 10 mini-trains, each capable of liquefying 0.3 million tonnes per annum (MTPA) of LNG–or roughly 40 million cubic feet per day (MMcf/d) of natural gas. There’s just one train left to bring online…

Read More “KM Puts Elba Island Train #10 into Service – One Train Remains”

Two different trade unions are asking some great questions about Pennsylvania Gov. Tom Wolf’s plan to force the state to join the so-called Regional Greenhouse Gas Initiative (RGGI), a carbon tax on coal and gas-fired electric generating plants. For example, how would a $2.36 BILLION carbon tax reduce carbon dixoide emissions any more than is already happening by the use of natural gas? PA already reduced CO2 emissions by 32% over the same time period RGGI (a coalition of liberal northeastern states) began–far more of a reduction than RGGI states have experienced!–without belonging to the RGGI tax plan.

Two different trade unions are asking some great questions about Pennsylvania Gov. Tom Wolf’s plan to force the state to join the so-called Regional Greenhouse Gas Initiative (RGGI), a carbon tax on coal and gas-fired electric generating plants. For example, how would a $2.36 BILLION carbon tax reduce carbon dixoide emissions any more than is already happening by the use of natural gas? PA already reduced CO2 emissions by 32% over the same time period RGGI (a coalition of liberal northeastern states) began–far more of a reduction than RGGI states have experienced!–without belonging to the RGGI tax plan.

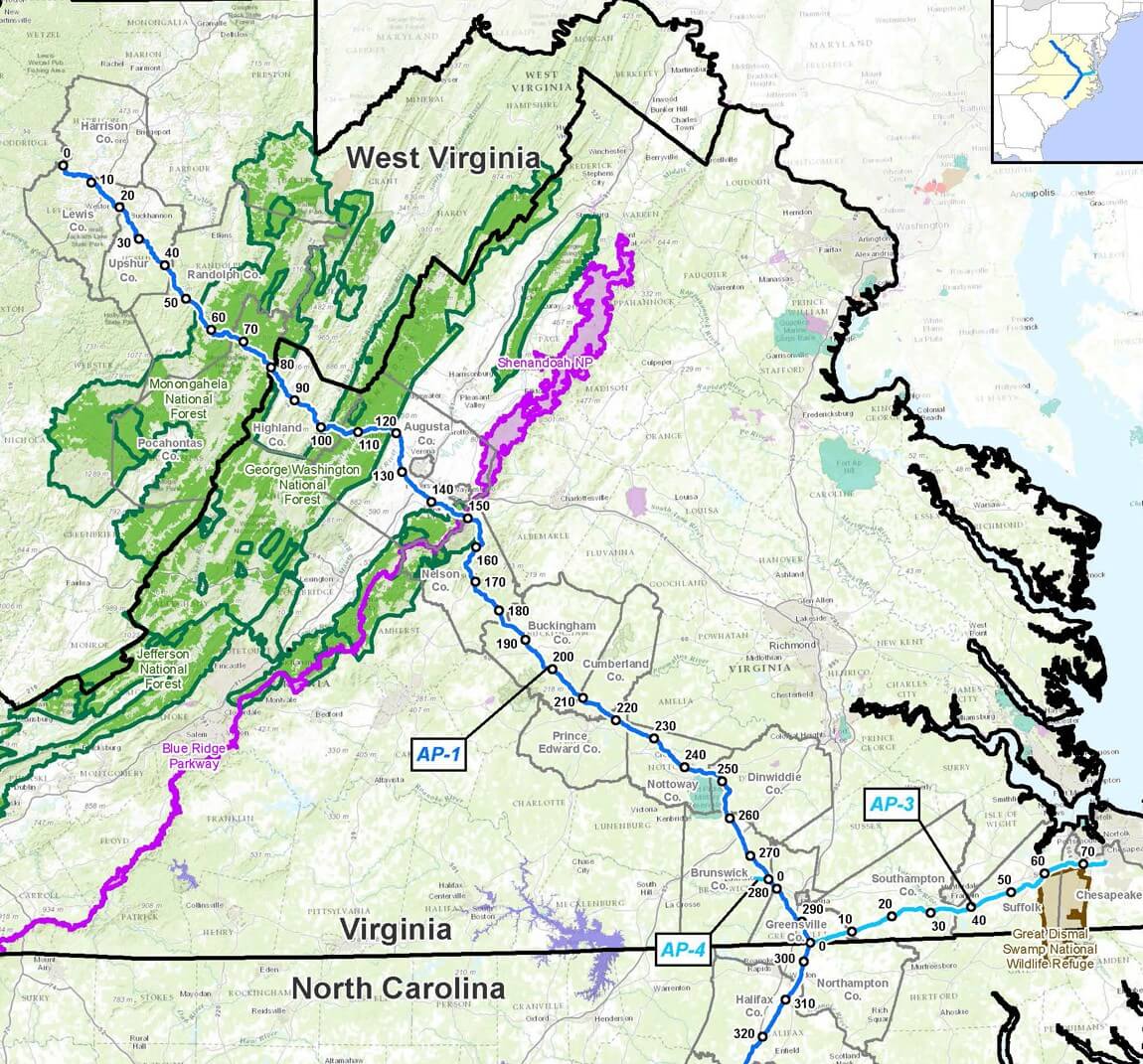

It’s been a loooong road getting the Mariner East 2 (ME2) pipeline system, which includes building two pipelines side-by-side from eastern Ohio across Pennsylvania to the Philadelphia area, done. From what we can tell, ME2 is now done–with the possible exception of a few miles where smaller pipeline is being used until a bigger replacement is done. For all intents, ME2 is done. However, ME2X, a second pipeline being built next to the first, is not yet done. But it’s getting close! According to comments from Energy Transfer (ET) made during a quarterly conference call yesterday, ME2X will be in service by the end of this year, and the entire project will be done-done sometime in 2Q21. Finally!

It’s been a loooong road getting the Mariner East 2 (ME2) pipeline system, which includes building two pipelines side-by-side from eastern Ohio across Pennsylvania to the Philadelphia area, done. From what we can tell, ME2 is now done–with the possible exception of a few miles where smaller pipeline is being used until a bigger replacement is done. For all intents, ME2 is done. However, ME2X, a second pipeline being built next to the first, is not yet done. But it’s getting close! According to comments from Energy Transfer (ET) made during a quarterly conference call yesterday, ME2X will be in service by the end of this year, and the entire project will be done-done sometime in 2Q21. Finally! Most of the layoffs during this particularly brutal (and historic) downturn in the oil and gas market have taken place in oilfield services companies like Halliburton, Baker Hughes and Sclumberger. But exploration & production companies are not immune. Chevron is laying off workers in their Marcellus/Utica operation because the company is selling all of its Appalachian assets and leaving the region (see

Most of the layoffs during this particularly brutal (and historic) downturn in the oil and gas market have taken place in oilfield services companies like Halliburton, Baker Hughes and Sclumberger. But exploration & production companies are not immune. Chevron is laying off workers in their Marcellus/Utica operation because the company is selling all of its Appalachian assets and leaving the region (see  In February MDN told you about an effort by the radicalized Sierra Club to block a New York landfill from accepting drill cuttings from the Pennsylvania Marcellus (see

In February MDN told you about an effort by the radicalized Sierra Club to block a New York landfill from accepting drill cuttings from the Pennsylvania Marcellus (see  We have some significant news coming out of yesterday’s 2Q update from Equitrans about the company’s Mountain Valley Pipeline (MVP) project. Equitrans is seriously considering expanding compression along MVP to flow an extra 500 million cubic feet per day (MMcf/d) of natural gas along the pipeline after it’s up and running.

We have some significant news coming out of yesterday’s 2Q update from Equitrans about the company’s Mountain Valley Pipeline (MVP) project. Equitrans is seriously considering expanding compression along MVP to flow an extra 500 million cubic feet per day (MMcf/d) of natural gas along the pipeline after it’s up and running. The Federal Energy Regulatory Commission (FERC) finally got its butt in gear and issued a favorable environmental assessment (EA) for an amended request by PennEast Pipeline to break the project into two phases–building the pipeline through Pennsylvania in Phase One, and through New Jersey in Phase Two. FERC was supposed to issue its findings on or by July 10. Finally, after two weeks with no report, no explanation, and no communication, PennEast goosed FERC on July 24 (see

The Federal Energy Regulatory Commission (FERC) finally got its butt in gear and issued a favorable environmental assessment (EA) for an amended request by PennEast Pipeline to break the project into two phases–building the pipeline through Pennsylvania in Phase One, and through New Jersey in Phase Two. FERC was supposed to issue its findings on or by July 10. Finally, after two weeks with no report, no explanation, and no communication, PennEast goosed FERC on July 24 (see  On August 1, 2019, Enbridge’s Texas Eastern Pipeline Company (TETCO) pipeline exploded in Lincoln County, Kentucky–killing one and sending six to the hospital (see

On August 1, 2019, Enbridge’s Texas Eastern Pipeline Company (TETCO) pipeline exploded in Lincoln County, Kentucky–killing one and sending six to the hospital (see

Range Resources has cut a deal to sell its Haynesville Shale assets (220,000 acres plus the wells they’ve drilled since buying those assets) to Castleton Resources, a privately owned company majority-owned by Tokyo Gas, for $245 million (plus an extra $90 million, maybe, contingent on the price of gas). Range bought those assets in 2016 for $4.4 billion (see

Range Resources has cut a deal to sell its Haynesville Shale assets (220,000 acres plus the wells they’ve drilled since buying those assets) to Castleton Resources, a privately owned company majority-owned by Tokyo Gas, for $245 million (plus an extra $90 million, maybe, contingent on the price of gas). Range bought those assets in 2016 for $4.4 billion (see  Yesterday the price of natural gas trading on the NYMEX futures exchange, a price based on the spot price at the Louisana Henry Hub trading point, zoomed up, closing 30 cents higher than the trading day before (up 14%). There does not appear to be a single, specific reason why trading took off like wildfire. Some speculate it rose based on the good news that U.S. LNG exports are once again on the rise. Others say short-term forecasts are now predicting continued hot weather. Whatever the reason, we’ll take it!

Yesterday the price of natural gas trading on the NYMEX futures exchange, a price based on the spot price at the Louisana Henry Hub trading point, zoomed up, closing 30 cents higher than the trading day before (up 14%). There does not appear to be a single, specific reason why trading took off like wildfire. Some speculate it rose based on the good news that U.S. LNG exports are once again on the rise. Others say short-term forecasts are now predicting continued hot weather. Whatever the reason, we’ll take it!