EIA Says Plenty of Gas Turbines for Data Centers in Ariz. Boneyard

As data center operators have sought rapidly deployable power sources for their facilities, some have turned to companies that modify jet engines for commercial power generation. Data center facilities in Texas have recently deployed modified jet engines as generators, each with 48 megawatts (MW) of generating capacity. There’s a whole “graveyard” of retired military aircraft at the U.S. Air Force’s facility on Davis-Monthan Air Force Base in Arizona, called the Boneyard. Could the old/retired jets at the Boneyard be repurposed to power data centers? Quite possibly! Read More “EIA Says Plenty of Gas Turbines for Data Centers in Ariz. Boneyard”

As data center operators have sought rapidly deployable power sources for their facilities, some have turned to companies that modify jet engines for commercial power generation. Data center facilities in Texas have recently deployed modified jet engines as generators, each with 48 megawatts (MW) of generating capacity. There’s a whole “graveyard” of retired military aircraft at the U.S. Air Force’s facility on Davis-Monthan Air Force Base in Arizona, called the Boneyard. Could the old/retired jets at the Boneyard be repurposed to power data centers? Quite possibly! Read More “EIA Says Plenty of Gas Turbines for Data Centers in Ariz. Boneyard”

Global LNG markets are entering a transitional phase in 2026, characterized by a projected 10% supply surge as major U.S. and Qatari projects come online. This influx ends post-Ukraine war tightness of supply in the LNG market and will likely depress global prices to under $10 per mmBtu. Lower prices are expected to stimulate demand recovery in price-sensitive markets like China and India, while Europe increases imports to phase out Russian gas and replenish inventories. Although supply abundance benefits consumers, narrowing price spreads will likely squeeze U.S. export margins. Consequently, the industry is shifting toward ample availability and reshuffled trade flows through 2029.

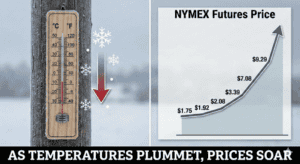

Global LNG markets are entering a transitional phase in 2026, characterized by a projected 10% supply surge as major U.S. and Qatari projects come online. This influx ends post-Ukraine war tightness of supply in the LNG market and will likely depress global prices to under $10 per mmBtu. Lower prices are expected to stimulate demand recovery in price-sensitive markets like China and India, while Europe increases imports to phase out Russian gas and replenish inventories. Although supply abundance benefits consumers, narrowing price spreads will likely squeeze U.S. export margins. Consequently, the industry is shifting toward ample availability and reshuffled trade flows through 2029.  Old Man Winter has proven once again that he is the one in charge of natural gas prices. A cold blast now entering the Midwest and Northeast, which is moving in until early February (at least), is the reason for a dramatic jump in the NYMEX front-month futures contract price, rising 80.4 cents per MMBtu (26%) in one day, yesterday, to a closing price of $3.9070 MMBtu. It is the largest one-day percentage gain in four years, since January 2022. The price continued climbing this morning (Wednesday) and looks like it might flirt with $5.00!

Old Man Winter has proven once again that he is the one in charge of natural gas prices. A cold blast now entering the Midwest and Northeast, which is moving in until early February (at least), is the reason for a dramatic jump in the NYMEX front-month futures contract price, rising 80.4 cents per MMBtu (26%) in one day, yesterday, to a closing price of $3.9070 MMBtu. It is the largest one-day percentage gain in four years, since January 2022. The price continued climbing this morning (Wednesday) and looks like it might flirt with $5.00!  On Friday, the White House joined with the 13 governors whose states in whole or in part are served by the PJM Interconnection electric grid, the largest grid in the country, to propose a solution that “protects consumers” from soaring electric rates due to the addition of new AI data centers (see

On Friday, the White House joined with the 13 governors whose states in whole or in part are served by the PJM Interconnection electric grid, the largest grid in the country, to propose a solution that “protects consumers” from soaring electric rates due to the addition of new AI data centers (see  As MDN reported, on Friday, the Trump administration officials joined several governors from states that are part of the PJM Interconnect grid to outline a broad plan they say will ensure customers of the grid (the country’s largest grid), will not face skyrocketing electric prices due to new AI data centers getting built in the region (see

As MDN reported, on Friday, the Trump administration officials joined several governors from states that are part of the PJM Interconnect grid to outline a broad plan they say will ensure customers of the grid (the country’s largest grid), will not face skyrocketing electric prices due to new AI data centers getting built in the region (see  The Marcellus/Utica rig count gained 1 rig six weeks ago in the Ohio Utica, bringing the total to 39 rigs. For the past six reports in a row, the M-U has maintained that count—the most rigs it has operated in more than a year. Pennsylvania has held at 18 active rigs for nine consecutive weeks. Ohio has operated 14 rigs for six straight weeks (its highest in over a year). And West Virginia maintained 7 rigs, which it has operated since May 30, 2025. There were 24 rigs targeting the Marcellus and 15 targeting the Utica. The national count lost 1 rig last week, bringing the total down to 543 active rigs.

The Marcellus/Utica rig count gained 1 rig six weeks ago in the Ohio Utica, bringing the total to 39 rigs. For the past six reports in a row, the M-U has maintained that count—the most rigs it has operated in more than a year. Pennsylvania has held at 18 active rigs for nine consecutive weeks. Ohio has operated 14 rigs for six straight weeks (its highest in over a year). And West Virginia maintained 7 rigs, which it has operated since May 30, 2025. There were 24 rigs targeting the Marcellus and 15 targeting the Utica. The national count lost 1 rig last week, bringing the total down to 543 active rigs.

We recently became aware of an Ohio Supreme Court decision that affects producers (i.e., drillers) and, by extension, potentially affects royalties for landowners and rights owners. In E. Ohio Gas Co. v. Croce, the Supreme Court affirmed that the Public Utilities Commission of Ohio (PUCO) has exclusive jurisdiction over claims brought by natural gas producers against Dominion Energy. The producers alleged conversion and unjust enrichment, claiming Dominion sold their excess gas without compensation. The producers tried to litigate the matter in the courts. But the Supreme Court ruled that, in these types of cases, PUCO has primary jurisdiction—not the courts.

We recently became aware of an Ohio Supreme Court decision that affects producers (i.e., drillers) and, by extension, potentially affects royalties for landowners and rights owners. In E. Ohio Gas Co. v. Croce, the Supreme Court affirmed that the Public Utilities Commission of Ohio (PUCO) has exclusive jurisdiction over claims brought by natural gas producers against Dominion Energy. The producers alleged conversion and unjust enrichment, claiming Dominion sold their excess gas without compensation. The producers tried to litigate the matter in the courts. But the Supreme Court ruled that, in these types of cases, PUCO has primary jurisdiction—not the courts.  Wow, talk about strange bedfellows! On Friday, the White House joined the 13 governors whose states in whole or in part are served by the PJM Interconnection electric grid, the largest grid in the country, to propose a solution that “protects consumers” from soaring electric rates due to the addition of new AI data centers. While some of the ideas discussed were good, others (such as an anti-capitalist price cap) were not. We’ll explain.

Wow, talk about strange bedfellows! On Friday, the White House joined the 13 governors whose states in whole or in part are served by the PJM Interconnection electric grid, the largest grid in the country, to propose a solution that “protects consumers” from soaring electric rates due to the addition of new AI data centers. While some of the ideas discussed were good, others (such as an anti-capitalist price cap) were not. We’ll explain.  Last week, the EPA proposed a new rule (copy below) to restrict states’ and Native American tribes’ ability to block major projects, such as pipelines and data centers, by abusing the Clean Water Act. By narrowing Section 401 reviews to focus solely on direct water pollution, the Trump administration seeks to accelerate fossil fuel infrastructure and AI development through increased regulatory predictability. This move reverses Biden-era policies that allowed for never-ending environmental evaluations. While administration officials argue these constraints prevent unnecessary delays, environmental radicals contend the proposal undermines local authority to protect drinking water and ecosystems. A final rule is expected this spring.

Last week, the EPA proposed a new rule (copy below) to restrict states’ and Native American tribes’ ability to block major projects, such as pipelines and data centers, by abusing the Clean Water Act. By narrowing Section 401 reviews to focus solely on direct water pollution, the Trump administration seeks to accelerate fossil fuel infrastructure and AI development through increased regulatory predictability. This move reverses Biden-era policies that allowed for never-ending environmental evaluations. While administration officials argue these constraints prevent unnecessary delays, environmental radicals contend the proposal undermines local authority to protect drinking water and ecosystems. A final rule is expected this spring.  The U.S. Energy Information Administration (EIA) predicts U.S. electricity generation will reach 4,423 billion kilowatthours by 2027, driven by steady annual growth. That’s up 3.7% from 4,260 billion KWH in 2025. While natural gas remains the primary power source, its market share is slipping alongside coal, which is declining 5% annually due to plant retirements. Dispatchable (on-demand) sources of electricity generation (natural gas, coal, and nuclear) accounted for 75% of total generation in 2025, but EIA expects their share to fall to about 72% in 2027. EIA expects the combined share of generation from solar and wind power (unreliable renewables) to rise from about 18% in 2025 to about 21% in 2027. Renewables are still minuscule compared to dispatchable natural gas and coal—which is as it should be if you care anything about energy security.

The U.S. Energy Information Administration (EIA) predicts U.S. electricity generation will reach 4,423 billion kilowatthours by 2027, driven by steady annual growth. That’s up 3.7% from 4,260 billion KWH in 2025. While natural gas remains the primary power source, its market share is slipping alongside coal, which is declining 5% annually due to plant retirements. Dispatchable (on-demand) sources of electricity generation (natural gas, coal, and nuclear) accounted for 75% of total generation in 2025, but EIA expects their share to fall to about 72% in 2027. EIA expects the combined share of generation from solar and wind power (unreliable renewables) to rise from about 18% in 2025 to about 21% in 2027. Renewables are still minuscule compared to dispatchable natural gas and coal—which is as it should be if you care anything about energy security.  The rumor mill is in overdrive today with news that Coterra Energy is in serious talks with Devon Energy exploring a potential merger “that would be among the biggest oil and gas deals in years.” While the primary driver of this deal is gaining massive scale in the Permian Basin, Coterra’s substantial Marcellus Shale assets in northeastern Pennsylvania (NEPA) are a major point of speculation for analysts and investors. It appears possible (likely?) that a combined company would sell off the PA Marcellus assets.

The rumor mill is in overdrive today with news that Coterra Energy is in serious talks with Devon Energy exploring a potential merger “that would be among the biggest oil and gas deals in years.” While the primary driver of this deal is gaining massive scale in the Permian Basin, Coterra’s substantial Marcellus Shale assets in northeastern Pennsylvania (NEPA) are a major point of speculation for analysts and investors. It appears possible (likely?) that a combined company would sell off the PA Marcellus assets.  Sorry, Field of Dreams, but if you build it, they don’t necessarily come. That’s the hard lesson for one of the biggest boondoggles of the Biden years—seven hydrogen hub projects (from 33 finalists) promised a collective $7 billion in federal funding (see

Sorry, Field of Dreams, but if you build it, they don’t necessarily come. That’s the hard lesson for one of the biggest boondoggles of the Biden years—seven hydrogen hub projects (from 33 finalists) promised a collective $7 billion in federal funding (see  JobsOhio, a private, nonprofit corporation that works on behalf of the state to drive job creation and new capital investment in Ohio by attracting business, contracts its economic research to Cleveland State University (CSU) to keep tabs on the Utica Shale industry. JobsOhio released the latest CSU updated report earlier this week (full copy below), showing that more than $114.6 billion has been invested in Ohio across natural gas, natural gas liquids, and petrochemical supply chain industries since 2011. Ohio’s shale energy sector drew approximately $3.5 billion in fresh capital between July and December 2024.

JobsOhio, a private, nonprofit corporation that works on behalf of the state to drive job creation and new capital investment in Ohio by attracting business, contracts its economic research to Cleveland State University (CSU) to keep tabs on the Utica Shale industry. JobsOhio released the latest CSU updated report earlier this week (full copy below), showing that more than $114.6 billion has been invested in Ohio across natural gas, natural gas liquids, and petrochemical supply chain industries since 2011. Ohio’s shale energy sector drew approximately $3.5 billion in fresh capital between July and December 2024.  Duke Energy is considering constructing a 1,360-megawatt natural gas power plant on 1,600 acres in Davidson County, North Carolina. This is the first we’ve heard of this project, and judging by our research, the first anyone has heard of it. Prior to this, we were aware of two Duke gas-fired projects in N.C.—one in Person County and one in Catawba County (see

Duke Energy is considering constructing a 1,360-megawatt natural gas power plant on 1,600 acres in Davidson County, North Carolina. This is the first we’ve heard of this project, and judging by our research, the first anyone has heard of it. Prior to this, we were aware of two Duke gas-fired projects in N.C.—one in Person County and one in Catawba County (see